Oct 31, 2018 | Press Releases

Odyssey Capital Group Ltd is pleased to announce that the Odyssey Japan Private Equity Real Estate division has been selected by Shinhan Investment Corp (a division of Shinhan Financial Group) to be their Japan Hospitality Advisor and Fund Manager for an institutional mandate.

The joint venture will allow Shinhan’s clients to benefit from Odyssey’s Japan Hospitality investment strategy, which includes seeking investments in boutique hotels, Ryokan’s (Traditional Japanese Inns) and Machiya’s (Traditional Japanese Townhouses) in the Kansai region and other areas of Japan. The investment model is to acquire, re-position and operate. By deploying a value-add strategy, Odyssey aims to increase the value of the assets acquired both at the asset level and the operational level. Odyssey’s goal is to increase the value of the underlying assets through a combination of property enhancements and improving the operational efficiencies of the underlying assets.

On the back of its strong and stable corporate governance and financial structure, Shinhan Investment Corp is fast emerging as a leader in Korea’s securities industry and provides securities trading, wealth management, and investment banking services, mergers and acquisitions, investment trusts, and corporate financing services. Shinhan Investment serves clients worldwide and is a subsidiary of Shinhan Financial Group, the second largest Bank in South Korea. Shinhan is, historically, the first bank in Korea, established in 1897 and now boasting more than 10,000 employees with more than US$260 billion in total assets.

Coinciding with the partnership between Odyssey and Shinhan is the initial acquisition of an attractive boutique hotel in Kyoto, Hotel Owan (https://resistay.jp/en/room/owan-amaterrace/) with the closing completed on the Friday 26th of October.

Kyoto is the historical capital of Japan and, as a result, many of Japan’s greatest entertainers, artists, chefs, designers and architects have resided and honed their craft in and around the city.

Odyssey’s boutique hotel asset embodies Japanese traditional culture and combines traditional, historical, Kyoto-based design and art motifs with modern and funky, boutique construction. Hotel Owan has 19 rooms which spread across 4 floors and comprise 8 wholly unique styles to cater to all types of affluent taste, whether they be for a room that includes tatami floor space, or one fitted with spacious, family-sized, double bunk beds or sleek and minimalist rooms for couples. With traditional Kyoto crafts, such as Nishijin fabric, and delicately featured interiors, you can feel an authentic beautiful Kyoto experience during your stay.

The appeal for local and foreign guests is well established as Hotel Owan has operated at an occupancy rate above 80% since it’s opening in 2017 and frequently experiences periods of 100% occupancy with consistent, ubiquitous, rave reviews on its quality of construction and design, it’s feel and styling and its central location and service.

Odyssey’s Japan Real Estate investment team, led by Christopher A. Aiello, was able to acquire the asset at a below market price and felt that current market demand will allow for increasing Average Daily Room Rates (ADR’s) by 20% to 25% over the next 12 months. Odyssey also plans to add concierge service upgrades and also employ a focused and upgraded digital marketing and direct bookings strategy.

The Managing Director of Odyssey Japan CRE, Christopher Aiello said, “We are excited to have completed the acquisition of this wonderful boutique hotel today. We have been able to secure this asset over other bidders due to the long term vision we have for the Japanese Boutique Hospitality industry, the strength of the Odyssey team and our seasoned relationships in Japan. We were able to secure a very attractive debt package for this acquisition from Mitsublishi UFG, one of the leading banks in Japan with an LTV ratio of 65%, non-recourse debt, and with an annual cost of 1.6% pa.”

Odyssey has long-term working relationships with the top leading individuals and firms in the Japanese commercial real estate and hospitality market and these partnerships include our panel banks, trust institutions, local asset managers, legal counsel, tax specialists and accountancy professionals.

The Odyssey CRE team commenced operations in early 2017 in Japan, and its well established and deep local presence, networks and insights allowed for the identification of the best and most appropriate real estate opportunities for the Odyssey Japan Hospitality strategy. Since this time, the Manager has reviewed more than 50 assets and has built up a robust pipeline.

The Odyssey Japan Real Estate investment team looks forward to providing our valued clients with more unique and exciting opportunities in what, we believe, will be one of the most successful Japanese hospitality investment projects to date. Please contact Odyssey, should you be interested in investing in Japanese real estate.

Odyssey Asset Management Limited

Odyssey Asset Management Ltd, a sister company to the Odyssey Capital Group, is a Hong Kong SFC 1, 4 & 9 licensed company. The Japanese CRE team is headed up by Christopher A. Aiello, and also includes Alex Walker, Daniel Vovil and Sam Luck.

Odyssey Capital Group Ltd is Asia’s leading independent Alternative Asset Manager that provides differentiated and bespoke investment solutions across multiple asset classes, including asset management, real estate, private equity and hedge funds. The Firm’s primary focus is to seek out undervalued investment opportunities to co-invest in with its clients.

The Odyssey team comprises over 30 experienced executives, asset managers, lawyers, private bankers, trust & tax planning specialists and experienced investors with over 400 years of combined financial and operational experience across the Asia Pacific, Europe and North America.

If you would like to learn more about Owan Hotel or if you would like to learn about our upcoming property purchases, please get in touch with us at: japan@odysseycapital-group.com

For more information about the Odyssey Japan Boutique Hospitality Fund, phone or email Daniel Vovil via the contact details listed below.

Daniel Vovil, Co-Founder and President, Odyssey Capital Group

daniel.vovil@odysseycapital-group.com | (852) 9725-5477

Oct 9, 2018 | Articles, Global Markets Update

More US Trade tariffs on China, Italy’s debt problem, the Federal Open Market Committee (FOMC) meeting, Liberal Democratic Party (LDP) leadership and Sweden’s election all made September an interesting month for news, but most had a relatively little impact across risk assets over the month.

However, there was significant inter-month volatility in some asset classes and currencies. Italy surprised complacent markets by announcing an irresponsible 2019 budget with increased spending that contradicted the European Union’s (EU) requirement that Italy cuts its debt-to-GDP to 60% from its present 130%. Sweden’s election maintained the form seen elsewhere in EU, with populist parties gaining huge ground but not political power – Italy is the exception. In equities, the S&P 500 ground higher but ‘growth-y’ sectors underperformed relative to defensives, as seen by the fact Nasdaq fell 0.8% against S&P 500’s modest gain of 0.4%. Compared to the last quarter, S&P 500’s gain of c. 7% is the best quarterly gain since 2013. Nikkei was a standout, up 5.5% and 8% from the last month and the last quarter respectively. Robust earnings, Abe’s victory in the LDP leadership battle, and a weaker JPY were the main contributors. A-shares recovered further from its recent two-year low by 3.5%, to head towards testing a 3,000 resistance, but Asia-ex Japan (AXJ) was the standout faller, losing 1.6% on trade concerns, earnings downgrades and FX weakness.

We see the sell-off in Emerging Markets (EM) as an opportunity to switch out of more expensive US equities into AXJ equities and to add to EM local currency debt. We would not rush – trade war escalation could well happen in the short-term – but we fundamentally do not ‘buy’ the EM crisis thesis, do not think US equities have ‘immunity’ to the risks out there that other equity markets have discounted and do not think the world goes into recession. Tactically, in terms of portfolio positioning, we think inaction might be better than action in the short-term given rising geopolitical risks. Poor EM Q3 earnings could well be another catalyst for EM equities to lurch down. In Developed Markets (DM), there is a case to slowly shift exposure in U.S. equities to cheaper European and Japan equities.

Equities

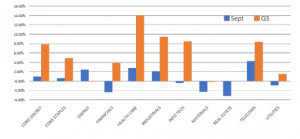

- In the US, we have seen an impressive Q3 as equities benefited from strong Q2 earnings releases, accelerating macroeconomic data and the presumption that U.S. equities offered some ‘immunity’ to trade wars. Sector rotation saw financials, real estate, materials, and utilities all fall while healthcare, telcos, and energy outperformed. Over Q3, the big winner was health care at +14% with energy, materials and real estate all down and financials underperforming along with consumer staples (Fig 1).

Fig 1. Monthly and quarterly performance of SPX sectors Source: Bloomberg

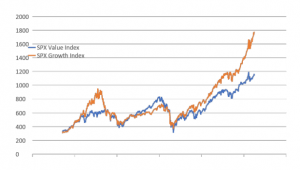

Fig 2. SPX Value vs Growth Source: Bloomberg

- The focus will be on upcoming Q3 results later this month, as late cycle and slowing earnings growth suggests defensive sectors and energy might outperform ‘growth’ and bond ‘proxies’. ‘Value’ stocks are close to record lows against growth (Fig 2) and we are potentially moving into an environment that value tends to do better in.

- In the EU, Stoxx and FTSE 100 are being moved around by politics and links to currencies. Italy may weigh on EU assets and Euro this month. 15th is the key date when details on the budget are revealed, and the fear is its spending plans might be multi-year. The EU financial system is inextricably linked to Italy’s fate given its debt pile is the second largest in size and its feeble GDP growth is not sufficient to reduce the debt let alone add to the debt. Our base case remains a compromise between Italy and EU but this might take time given the coalition’s political strength.

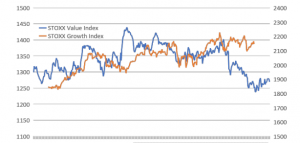

- Morgan Stanley (MS) thinks that European Equities are “unloved, under-owned and undervalued’ and recommends adding to exposures to overweight. Additionally, MS highlighted that value is at record lows to growth (Fig 3) and conditions suit a shift into value. Energy is seen as a late-cycle outperformer too.

Fig 3: STOXX Value vs Growth Source: Bloomberg

- In Asia, we saw the NIKKEI 225 soar almost 8% in Q3 to test multi-decade highs, while China A-shares recovered slightly by 3.5%, back above its support at 2,850 albeit helped by the Chinese government’s moves to reflate the domestic economy to mitigate trade damage from US tariffs, and by PBOC’s trenchant defense of CNY below 6.90.

- Nikkei’s surge may continue into Q4 on further positive earnings revisions, better macro data, and certainty of policy under Abe-Kuroda. China is facing the risk that the US, under Trump, is starting a new cold war of which trade is but one form of confrontation and containment. For Chinese equities, China’s moves to dial-back its aggressive de-leveraging, start to unfreeze the halted WMP sector and stabilize the CNY are all positive steps, but in the short term, Q3 results might be quite disappointing, especially in the consumer related space.

- It seems that in AXJ regions, central banks and governments are taking sensible steps in the face of a severe sell-off in FI and FX by raising interest rates, seeking to slow imports and allowing FX to weaken. In particular India, Indonesia and Philippines are raising rates and letting their currencies crash. This suggests these economies and markets will recover far faster once the pressure lifts, as it surely will, offering good value opportunities for patient investors.

Fixed-Income

- US Treasury yields broke through a multi-year high (Fig 4), with the 10y yield jumping 11bps to 3.18% after a raft of better-than-expected macro numbers came out last week. The 2Y10Y yield curve has also steepened a little too. Shorts on 10y UST are now at record highs.

Fig 4: UST 10Y yield hits 7Y high. Source: Bloomberg

- Whilst there were large outflows from DM government bonds last month (the most since February), EM Fixed-Income saw large inflows for the first time in several months and yields tightened quite sharply. This, despite lurid warnings of the degree corporate debt, has risen in EM since GFC, was obvious the buying was from larger institutions and sovereign wealth funds.

- The debate in where US Treasury yields may go from here is polarised between the bulls and the bears, with both sides having plausible arguments. The argument for higher inflation and a stronger USD assumes the US labor market is tightening to a point where wage inflation must accelerate fast, but that inflation expectations will remain anchored at what are historically unprecedented lows for far longer, is dangerously complacent. Bears think the opposite, and that there is sufficient slack in the labor force, the tick up in inflation is temporary, and the Fed is in danger of over-tightening, which might catalyze the next recession as soon as 2020. No one knows whether US labor markets are tighter than understood or has more slack than realized but we will find out sooner than later.

Currencies

- USD DXY fell below a key level at 95 as Draghi’s apparently ‘hawkish’ comments pushed Euro back above its 200DMA just above 1.18 and positive Brexit ‘noise’ helped GBP through 1.32 but this soon evaporated with Italy’s budget quickly unshackling Euro that promptly tested its key YTD support at 1.1515 whilst GBP tumbled back below 1.30 in part from the baleful specter of Boris stalking May in the Conservative party’s corridors of power.

- USD upside to continue for longer appears to be the direction recent FX forecast revisions are going, even if many still see a weaker USD against the EURO and JPY in the medium term. On the face of the evidence, the stronger-than-expected US economy and related Fed rate hikes against weaker data in EU and EM/AXJ and higher UST real yield differential is USD supportive, and there is still a lot of stale USD bears out there to take a contrarian stance against the Dollar.

Commodities

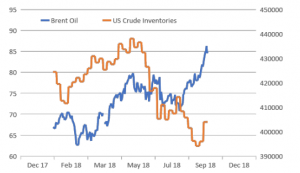

- The Brent Oil price soared 7% last month to $83/brl, and last week moved to YTD highs of over $86/brl despite a huge jump in US crude oil inventories (Fig 5) and a suggestion that Saudi Arabia and Russia might produce more to mitigate the likely supply reduction from Iran after US sanctions start 4th November.

Fig 5: Brent oil price is rising despite a recent jump in US inventories Source: Bloomberg, EIA

- Gold has traded flat in last month around $1,200/Oz after bouncing from support at $1,150/Oz – a level that saw a surge in physical gold buying by Asians, attracted by a lower cost, and a significant slowdown of speculative investors’ selling. Gold remains a by-product of USD moves, which many appear to prefer as the ‘safer’ haven asset.

- Oil prices will be driven by geopolitical risks – should Iran blockade the strategic Hormuz straits through which 40% of global seaborne oil is transported, we would see prices jump to $100/bpd in the short term. The medium-term too looks to be constructive for oil prices given estimates that demand will rise by 1.5mn/bpd over the next few years yet oil supplies might falter, in part after 60% cuts to oil E&P CapEx between H2CY14-’17. Reforms in the shipping industry to use less polluting fuel mixes will add to demand too. Several houses predict Brent oil at $100/brl by 2020.

CONTACT

We would be more than happy to have an informal chat about these and the other services we offer as well as the current opportunities we are looking at.