Apr 9, 2020 | Articles, Global Markets Update

Outlook

Despite heightened worries about the impact of the virus on the US, we believe data is consistent with our base case (60% probability) in which new virus cases peak by mid-April in Europe and the US; the most severe restrictions are lifted from May; and a coordinated monetary and fiscal response allows for a V-shaped recovery to take hold from the third quarter of this year with rapid acceleration in the fourth quarter. UBS “expects to see evidence by mid-month that the US is starting to bend the curve. In Europe, we see more compelling evidence that governments in Italy, Germany, France, and Spain are bending the curve now”.

Market developments over the coming weeks will hinge on four key factors: First, whether we see further evidence that containment measures are slowing infection rates. Second, whether announced government stimulus measures are actually succeeding in preventing job losses and bankruptcies. If governments can do this, then we could expect a relatively swift recovery in demand when economies reopen ie to ‘preserve capacity’. Thirdly central banks’ measures to prevent a liquidity crisis work in the next 2-3 months and thus stop a solvency crisis developing that might result in a severer recession or even a depression (and a far worse public healthcare crisis than this virus). Lastly evidence of a slowdown in infections and lower morbidity rates, as the use of better therapeutics make treatment more effective, should reduce fear and pessimism.

We believe markets are past the peak in panic seen in mid-March but very poor macro data, and the rising death toll, may mean we are not yet at maximum pessimism and that a retest of the 23rd March lows at 2,237 on SPX and 10year US Treasury yield at 31bps are quite possible and this fits with previous corrections needing markets to form a ‘double-bottom’. We would look to deploy cash and reposition defensive assets, as some of our Alternatives, into riskier assets into such declines.

With equities and lower quality bonds offering the most attractive valuations since 2016, higher risk investors can put excess cash to work via an averaging-in strategy. In addition, investors can buy gold as increasingly the only genuine ‘safe haven’ asset. We see opportunities in Asian equities that are relatively cheap and whose earnings impact from the virus is likely to be relatively limited, as well as quality stocks globally, that can protect dividend payments, that should be resilient.

We think credit is closer to pricing in our downside scenario than equities, and US investment grade, US high yield, and US dollar-denominated emerging market sovereign bonds all offer attractive opportunities after selling-off to levels last seen in the GFC. To put this into perspective US HY spreads over USTs blew-out by over 1,000bps, similar to the fall in GFC, which implies a 50% default rate over the next five years whereas SPX, using our estimates for ‘normalised’ earnings in FY21, is trading at just under 15x vs. the long-term 16.6x average and on over 2x PBV that is decent value but hardly a bargain. The explosive rally in equity markets late March means they are closer to pricing in our base case scenario and the need to be more selective. Equities main attraction is they look cheap relative to high quality bonds and offer better income too.

When to Downgrade the Lockdown?

A real concern is that unless economic activity is restored relatively quickly, companies with much reduced, or no, revenues will face a solvency issue and this risk is made worse by a record high debt to equity level that could lead to a Depression via a horrific credit crisis – surely a danger most governments would seek to avoid? We might not be able to contain the virus, but we can avoid triggering a solvency/credit crisis that may have other enormous public health consequences.

Perspective: Fullerton’s “letter”

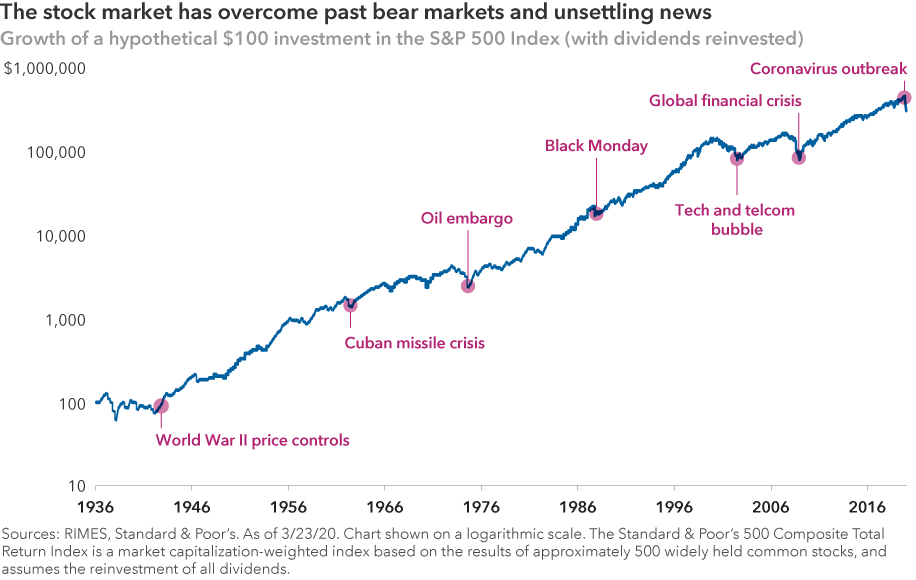

We will like to end this off with a speech from former Capital Group Chairman Jim Fullerton. He delivered this speech in Nov 1974 amid a prolonged bear market and provides us with a historical perspective, and some optimism, in a market environment like what we are in today.

Figure 1: Stock markets’ resilience Source: Capital Group

The speech is as follows:

“Courage! We have been here before”: One significant reason why there is such an extreme degree of bearishness, pessimism, bewildering confusion, and sheer terror in the minds of brokers and investors alike right now, is that most people today have nothing in their own experience that they can relate to, which is similar to this market decline. My message to you, therefore, is: Courage! We have been here before. Bear markets have lasted this long before. Well-managed mutual funds have gone down this much before. And shareholders in those funds and we the industry survived and prospered.

I don’t know if we have seen the absolute bottom of this prolonged bear market, (although I think we’ve seen the lows for a lot of individual stocks). Each economic, market and financial crisis is different from previous ones. But in their very difference, there is commonality. Namely, each crisis is characterized by its own new set of nonrecurring factors, its own set of apparently insoluble problems and its own set of apparently logical reasons for well-founded pessimism about the future.

Today there are thoughtful, experienced, respected economists, bankers, investors and businessmen who can give you well-reasoned, logical, documented arguments why this bear market is different; why this time the economic problems are different; why this time things are going to get worse — and hence, why this is not a good time to invest in common stocks, even though they may appear low. Today people are saying: “There are so many bewildering uncertainties, and so many enormous problems still facing us — both long and short term — that there is no hope for more than an occasional rally until some of these uncertainties are cleared up. This is a whole new ballgame.”

A whole new ballgame: In 1942 everybody knew it was a whole new ballgame. And it was. Uncertainties? We were all in a war that we were losing. The Germans had overrun France. The British had been thrown out of Dunkirk. The Pacific Fleet had been disastrously crippled at Pearl Harbor. We had surrendered Bataan, and the British had surrendered Singapore. In April 1942, inflation was rampant.

Today almost every financial journal or investment letter carries a list of reasons why investors are standing on the sidelines. They usually include (1) continued inflation; (2) illiquidity in the banking system; (3) shortage of energy; (4) possibility of further outbreak of hostilities in the Middle East; and (5) high interest rates. These are serious problems.

But on Saturday, April 11, 1942, The Wall Street Journal stated: “Brokers are certain that among the factors that are depressing potential investors are, (1) widening defeats of the United Nations; (2) a new German drive on Libya; (3) doubts concerning Russia’s ability to hold when the Germans get ready for a full-dress attack; (4) the ocean transport situation with the United Nations, which has become more critical; and (5) Washington is again considering either more drastic rationing with price fixing or still higher taxes as a means of filling the ‘inflationary gap’ between increased public buying power and the diminishing supply of consumer goods.” (Virtually all of these concerns were realized and got worse.)

On the same day, discussing the slow price erosion of many groups of stocks, a leading stock market commentator said: “The market remains in the dark as to just what it has to discount. And as yet, signs are still lacking that the market has reached permanently solid ground for a sustained reversal.” Yet on April 28, 1942, in that gloomy environment, in the midst of a war we were losing, faced with excess profits taxes and wage and price controls, shortages of gasoline and rubber and other crucial materials, and with the virtual certainty in the minds of everyone that once the war was over we’d face a post-war depression in that environment, the market turned around.

A return to reality: What turned the market around in April of 1942? Simply a return to reality. Simply a slow but growing recognition that despite all the bad news, despite all the gloomy outlook, the United States was going to survive, that strongly financed, well-managed U.S. corporations were going to survive also. The reality was that those companies were far more valuable than the prices of their stocks indicated. So, on Wednesday, April 29, 1942, for no apparent visible reason, investors again began to recognize reality.

The Dow Jones Industrial Average is not reality. Reality is not price-to-earnings ratios and technical market studies. Symbols on the tape are not the real world. In the real world, companies create wealth. Stock certificates don’t. Stock certificates are simply proxies for reality.

Now I’d like to close with this: “Some people say they want to wait for a clearer view of the future. But when the future is again clear, the present bargains will have vanished. In fact, does anyone think that today’s prices will prevail once full confidence has been restored?” That comment was made 42 years ago by Dean Witter in May of 1932 — only a few weeks before the end of the worst bear market in history. Have courage! We have been here before — and we’ve survived and prospered.

If you like to receive more information on our portfolios solutions, please contact us here: info@odysseycapital-group.com

Mar 24, 2020 | Articles, Global Markets Update

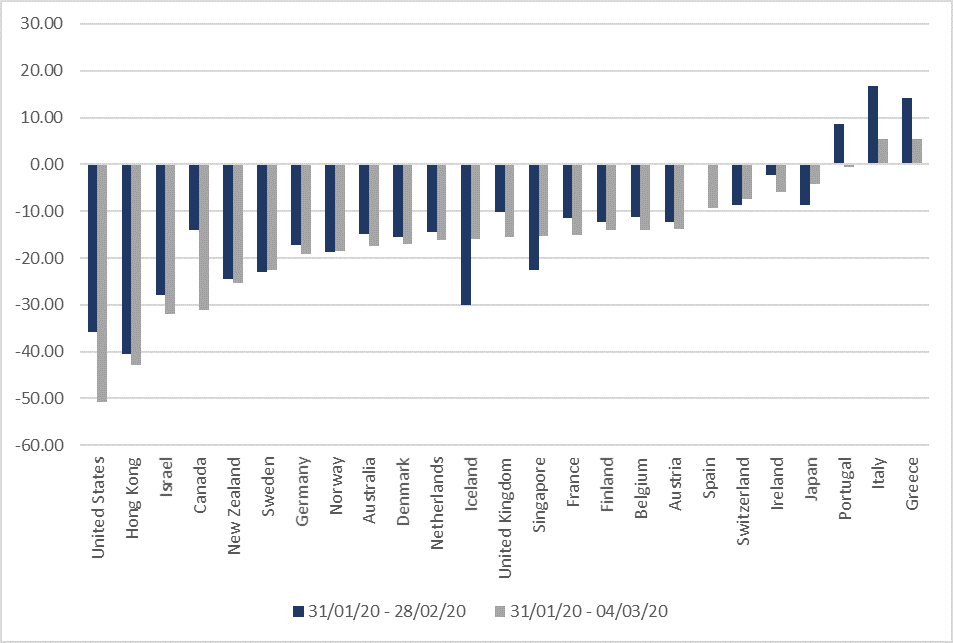

February was a tumultuous month for markets, which saw an elevated level of volatility across asset classes that extended even further into early March. Just as the coronavirus appeared to have come under some extent of control in China and other regions, Italy, South Korea and Iran quickly turned into hotbeds of infections and now increasingly, it looks like the rest of Europe and the U.S. will not be spared. Concern over how this would affect growth across these regions prompted a flight to safety, pushing the S&P 500 down -8.41% MoM, and sending the benchmark 10Y US Treasury Yield below 1% for the first time ever, and yields in Europe deeper into negative territory.

While equity markets were down across the board (the MSCI All-country World Index fell -8.21% MoM), the U.S. and Europe (the Stoxx 600 was down -8.54% MoM) saw a much steeper decline compared to their Asian counterparts like China A-shares (-3.22% MoM), the HSI (-0.69% MoM) and the broader MSCI Asia ex-Japan Index (-2.91%). The MSCI ASEAN Index (-9.29% MoM) underperformed, however, not least as markets grew concerned that this highly trade-dependent region would be significantly affected by a slowdown in global growth.

Understandably, oil prices also fell on similar concerns, with the price of Brent Crude off -13.14% MoM to US$58.16/bbl, sending Energy shares in the S&P 500 down -15.27%, and Oil & Gas names in the Stoxx 600 down -13.27% over the month.

On the U.S. political front, we saw Joe Biden take the DNC by storm, surprising markets with a strong comeback to take ten of the fifteen contests on Super Tuesday to prompt Bloomberg, Warren and Buttigieg to drop out of the race in quick succession to leave the contest between him and Bernie Sanders.

OUTLOOK

We are not supportive of a recession thesis in the U.S. nor globally, and do not think that we will be seeing a global pandemic. Our base case is that ‘this too shall pass’, but perhaps later than we had initially expected with the next four to six weeks being a tricky period as developed markets weigh the potential damage against reflation measures. Our sense is that the actual damage from the virus is far, far less than the fear of it but sooner than later fear will turn into realism. In our view, this pattern of behaviour might continue well into April.

Morgan Stanley’s strategists have opined a similar base case to mine, in that the virus will continue to spread into 1H20 before tapering off. In this case, global growth will likely see half a percentage point shaved off to c. 2.5%, but we will avoid a recession altogether. Their/our bull case scenario would see the spread taper off by late March, while the bear case sees it spreading well into 2H20 and thus result in global growth dropping to as low as -2.1% and a likely recession even if the Fed cuts by as much as 125bps. As such, anything less than the most drastic, worst-case scenario would suggest that the selloff will come to pass, and not indicative of the end of the cycle.

Having adopted a relatively conservative stance up to this point, we committed a portion of our cash pile last Friday when U.S. markets came off. We seek to cautiously use further dips to add to equities, and possibly high yield fixed Income if we see markets dip further. We see no reason to rush back into markets but will keep a close eye on technical indicators as opportunities to deploy capital might present themselves(Thursday’s fall took the S&P 500 a percentage point below Its 200DMA, with the Dow now 4.5% below, although Nasdaq remains above this level).

We expect further volatility as markets attempt to price in the short-term impact of the virus, effects of reflation in the medium to long-term, as well as political risks in the U.S. Over the next four the six weeks, however, it is more than likely that the virus will be the key driver. With the U.S. arguably being too complacent around the situation, they will undoubtedly go into high gear and exaggerate risks through far more draconian measures that will hurt sentiment – therefore we remain cautious in adding to U.S. equities.

We remain far more optimistic around China and the broader Asia ex-Japan region (bar South Korea), as they have adjusted to the situation and are now coming out the other side as infection rates slow, and markedly so in the case of China. Reflation in Asia ex-Japan seems to be more aggressive too – Singapore and Malaysia, for example, are boosting fiscal spending by a combined c. $9bn which is larger than the $8bn plus US Congress had earlier sought to pass.

Figure 1: A-shares outperformance towards end Feb Source: Bloomberg

We believe that the Fed has made a big error in cutting rates by 50bps, and this is a view that appears to be shares by quite a few others. There is no evidence that the US economy is or will be too badly damaged by the virus, especially after recent data releases which have been fairly supportive (ISM Manufacturing showed signs of recovery, while consumer data remained solid). A move like this comes across as more of trying to please the markets rather than being responsible, and to do it before Super Tuesday results were out beggars belief. The Fed has now used up a decent chunk of its ammunition, helped UST yields plunge to all-time lows, dumped the US Dollar and arguably created more worry than confidence as many might wonder why the Fed might make such moves. Fixed Income markets are now expecting 100bps of cuts in ’20 from just 25bps at the end of February.

This has sharply lowered the real interest rate differential USD had, and both the EUR & JPY reacted sharply to the Fed’s daft move, reigniting the latter’s ‘safe haven’ attributes which appeared to have been lost in last month’s selloff. With the virus spreading quickly into other developed markets, Japan’s poor handling of its spread is less of a negative. Indeed China and Singapore (Vietnam, too, has been quick to be strict on its approach) might be the exceptions, with other countries potentially far less able to handle an outbreak.

The collapse in yields – whilst probably good for mortgage refinancing and property demand – now suggests a deeply negative real rate. That suggests that FI markets think an imminent and severe recession may well be on its way soon, as compared to equity markets that are still not materially off all-time highs. This extreme dichotomy cannot last and my base case is that FI markets are exaggerating the risks, instead driving up bond prices to make the asset class effectively uninvestable bar short-term tactical trades.

This further underlines the relative attraction of cash vis-à-vis Fixed Deposits (3M LIBOR is now at 1% from 1.7% a month earlier), and also why we prefer to diversify into alternative income and alternatives more generally. We would consider looking at senior loans, on the basis that rates cannot get much lower (can they?) and have capped lower limits. Once things stabilize, the low base of US Treasury yields will further add to demand for positive yielding FI assets, not least High Yield bonds (The US HYG ETF is yielding 5.08%, thus providing a yield pick-up of over 4.2%). Having said that, there remains a concern around default risks jumping higher if the virus was to harm FCF generation, and not just the energy/oil-related CCC bonds either.

Figure 2: Chart showing DXY performance since 1994 Source: Bloomberg

In currencies, we wonder if this could be the inflection point for the US dollar. USD has plunged 3% WTD on the Fed’s move, with JPY storming back from the 110 level to test a key support at 105. EUR was also up sharply from its recent low of 1.0800. Both the ECB and BOJ may well ease next week/end March respectively, but probably along the lines of a 10bps cut compared to the Fed which some see cutting by a 100bps by the end of the year. Both Japan and the EU are likely to undertake far more expansive fiscal spending than the US might, given the high chance of partisan gridlock In the latter. If Germany was to abandon its idiotic zero deficit fiscal stance, this would boost EUR sharply. In our view, the DXY may have peaked at its 20Y high at c. 100.

![]()

![]()

![]()

![]() EQUITIES

EQUITIES

Markets in the US continued into all-time high territory throughout the most of February, though the tail end of the month into early March saw heavy selling amid Covid-19 concerns with the US starting to see its first few cases of the highly infectious virus. Last week was the S&P 500’s worst weekly decline since Oct ’08, with bank stocks taking a particularly hard beating (the widely-followed KBW bank index fell by as much as 20.7% from its Jan high) across a broader market selloff, and rising expectations of further rate cuts. Both the S&P 500 and Dow fell into a technical recession.

Figure 3: Performance of major US indices in Feb ’20 Source: Bloomberg

All sectors in the S&P 500 closed lower in the month of Feb, although defensive sectors like Telecommunications, Real Estate and Health Care were noticeably more resilient. Energy shares saw the steepest decline at -15.27%, extending January’s loss and weighed lower by a significant decline in oil prices which sold off on concern over a potential fall in global growth which would result in less demand.

Figure 4: S&P 500 sector returns in Feb ’20 Source: Bloomberg

Nevertheless, economic data showed some relative strength in the US economy, with University of Michigan’s US consumer sentiment survey coming in at 100.9 (vs est. 99.5), while retail sales rose 0.3% MoM in Jan to meet economists’ expectations. Headline PPI also beat estimates handily to rise 2.1% YoY in Jan (vs est. 1.6%). Home data was positive over the month, with new home sales up 7.9% in Jan to its strongest since mid ’07 on the back of cheaper borrowing costs, while home prices in 20 cities were up 2.85% YoY in Dec. Consumer confidence also edged higher in Feb to its best level in over half a year.

European markets were not spared from the bloodbath, not least with ECB chief economist’s warning that the coronavirus would be a ‘pretty serious short-term hit’ to Europe’s economy. The moves across indices were fairly similar, with all three major indices seeing a similar 8-9% move down alongside the Stoxx 600.

Figure 5: Performance of major European indices in Feb ’20 Source: Bloomberg

Within the Stoxx 600, all sectors saw losses although Oil & Gas and Travel & Leisure names took an understandably worse beating considering the outbreak compared to other sectors, although Basic Resources, Insurance, Media and F&B were not too far off. Notably, however, Utilities – often seen as a bond proxy and now more so given the rapid decline in bond yields – outperformed with only a -2.96% decline relative to the double-digit loss seen across sectors.

Figure 6: Stoxx 600 sector returns in Feb ’20 Source: Bloomberg

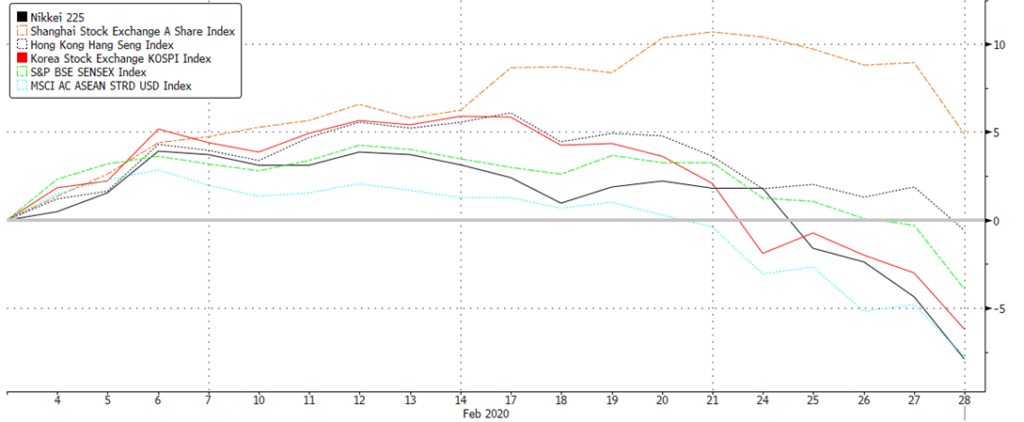

Most markets in Asia were also down, though much of the fallout had already happened over the course of January, and losses were relatively muted compared to indices in the US and Europe. The NIKKEI and MSCI ASEAN were the biggest losers in the region, falling -8.05% and -7.96% respectively. Perhaps in-line with the situation looking more contained in China and given the heavy selling which we saw earlier last month, China A-shares outperformed at +4.87% to be the only big index in this region to close positive this month.

Figure 7: Performance of major Asian indices in Feb’20 Source: Bloomberg

On the macroeconomic front, China also unveiled a string of easing measures including interest rates loans, injecting liquidity via reverse repos, and targeted tax cuts to small firms and the private sector. The PBoC is also slated to offer CNY 500b of lending and discounts to funding to commercial lenders for loans to small companies and the agricultural sector. The moves come amid China’s latest factory PMI for Feb, which fell to an all-time low of 35.7 (vs est. 45). Overall, we saw an increasing number of countries introduce a slew of easing measures, most notably so in Southeast Asia.

FIXED INCOME

There was a clear shift to quality in Feb as fears around COVID-19 plagued markets. 10Y sovereign yields in developed markets mostly fell through Feb and into first few days of March (Fig 8).

Figure 8: DM 10Y sovereign yields Source: Bloomberg

10Y UST yields led the decline, falling 36bps through Feb and a further 15bps in the first two trading days in March – a large part of it was caused by fears of a deeper Covid-19 outbreak. New cases and fatalities in the US, and in other countries outside China, led the FOMC to announce an emergency rate cut of 50bps on 3rd March. This led to the 10Y yield falling to a record low of 0.9043% intraday before easing higher to close 1.00% that same day (Fig 9). The 3M UST yield also fell to 0.70% at the close of 4th March – significantly below the Fed’s new policy rate range of 1% – 1.25%, while the 30Y yield fell to a record low of 1.61%. As of 3rd March, markets are pricing in an 84% probability of at least one more rate cut by YE20, and a 42% probability of at least two rate cuts.

Figure 9: 10Y UST falls to record low intraday Source: Bloomberg

Over in Europe, sovereign yields were also pressured lower, especially in Italy after the number of reported Covid-19 cases in the country spiked up. After warning of the virus’ short-term impact on Europe’s economy, ECB Chief Economist Philip Lane said the new normal for ECB rates ranged somewhere between zero and 3% while Bank of Spain’s governor Pablo Hernandez de Cos said the bank should adopt an inflation target of 2%. Markets are also pricing in one cut by ECB in July. ECB president Lagarde downplayed the likelihood of ECB providing an immediate response to the outbreak earlier in Feb, but the Fed’s recent move might likely pressure the ECB into cutting, potentially sending rates further into negative territory.

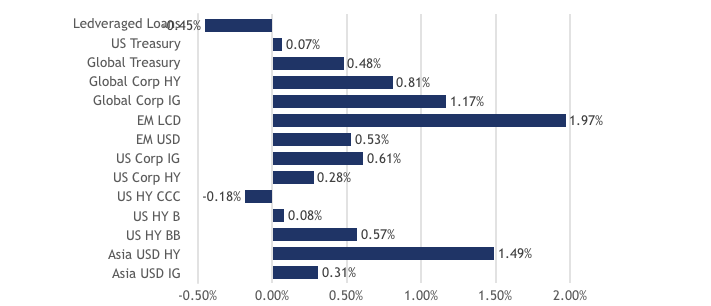

The flight to safety was prevalent in the credit space too. The amount of inflows into IG was significant, thus capping the spread widening and leading the sector to outperform HY credit. Global and US IG index spreads were narrowing to their lowest in early ’18 before widening again towards the end of Feb when Covid-19 induced fears resurfaced (Fig 10). The spread widening was more significant in the HY, with global HY index spreads widening to levels last seen in ’16. This led to the spread between IG and HY widening too, with the BBB/BB spread moving form a record low 38bps to 150bps. Ultimately, the higher coupons in HY will offset the spread widening in the lower quality segment of the market but bottom up credit selection is important – we recommend avoiding certain sectors like Energy and Gaming, which might see significant impact in the near-term from the virus outbreak.

Figure 10: Global IG and HY spreads widden amid Covid-19 fears Source: Bloomberg

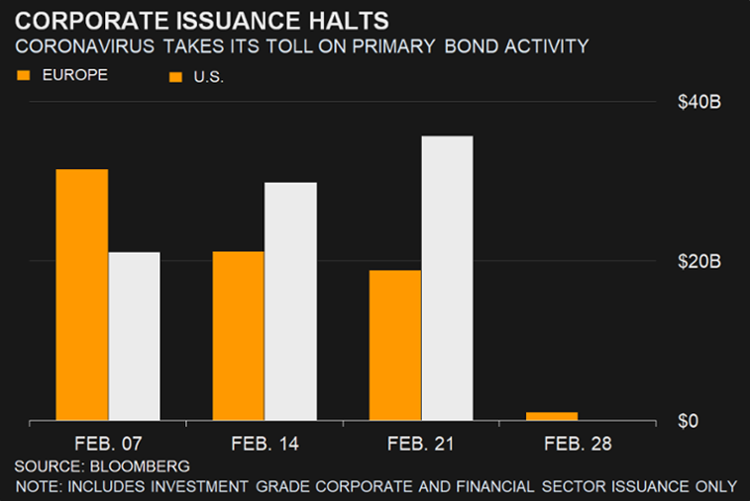

Issuance during the last week of Feb, especially in IG, also came to a standstill as companies held off in the face of the virus induced sell off (Fig 11). Technical indicators might be supportive of the asset class in general in the near-term as uncertainty around the severity of the Covid-19 outbreak. There is even an argument to buy credit now that spreads have widened significantly enough for there to be some insurance. In the longer term, rates are likely going to stay lower for longer with inflation unlikely to come back anytime soon.

Figure 11: IG issuance comes to a standstill Source: Bloomberg

FX

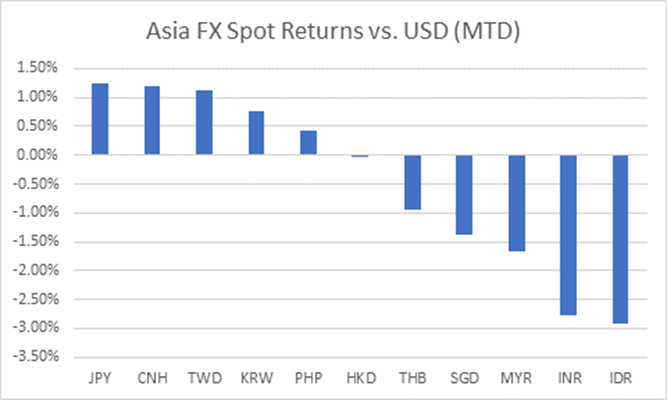

This month saw FX volatility spike at its quickest pace since the Sino-US flareups – Asian currencies bore the full brunt of the damage earlier in the month as trade-related data in the APAC region fell at a record pace amidst concerns of an elongated disruption in the supply chain.

As the infection rate climbed in South Korea, Iran, Italy and Japan, risk-off sentiments continued to dampen markets causing once-favoured carry trades such as the IDR and INR to unwind. Investors then sought the JPY as a haven while the CNY remained resilient from its aggressive reflation (Fig 1).

Adding to our previous point, the Federal Reserve unexpectedly lowered interest rates by 50bps in the beginning of March, causing mixed reactions to the drastic move. This caused the dollar to reverse its gains, relieve the KRW’s pressure and further boosted JPY as it continued to pare its losses from 112.23 to 106.85.

We foresee weakness in the USD, and further weakness in the INR and IDR as we believe these countries remain at the highest risk due to its lack of infrastructure spending as well as population density.

We remain positive on CNH as we continue believe there is further room for the PBoC to reflate its economy and that markets have already priced in a much lower 1Q GDP reading. We also remain bullish on JPY and SGD as they stand to benefit the most from the Fed’s recent rate cut.

Figure 12: Asian currencies fell hard in Feb Source: Bloomberg

COMMODITIES

The Brent oil price continued its selling momentum from January as global growth continued to reel from the coronavirus. Oil fell a total of -15.60% and remained above its key support of $50. It ended the month at $52/barrel. Gold continued to gain from its haven attributes and touched a 7-year high of $1,689/oz.

Our view remains unchanged – a slowdown in global growth will continue to be the main headwind for Oil and as a catalyst for Gold. Automobile sales around the world has slowed down with China’s automobile purchases almost coming to a halt as a recent report from the PCA is showing car sales falling by over 80%.

We continue to believe that $50 is a strong support for Oil based on two factors; global reflation led by China and a supply cut from OPEC+ members in the near-distant future. Of the two factors mentioned, in the short term, we argue that Saudi Arabia’s proposal of a further 1.5-million-barrel cut remains unlikely. Our belief is that OPEC+’s rate of participation remains hard to quantify as investors are expecting a certain amount of reluctancy from Russia and Iran.

We continue to see limited upside for Gold for the same reason that Oil will see further upside; global reflation and markets being accustomed to the coronavirus’s rate of infection. We believe that the inflection point is located at $1,600/oz, a key support level for Gold. As the initial shock of the coronavirus is now over, we see Gold trading on fear and uncertainty rather than panic, seen by Gold since it rose from $1,480.

Feb 11, 2020 | Articles, Global Markets Update

Markets were risk on at the start of January on the back of optimism around the successful signing of the US-China phase one deal and the easing of US-Iran tensions. However, that was quickly forgotten and reversed following the coronavirus outbreak, which led to an extended holiday in China and the cancellation of several inbound flights to China by multiple airlines. Fears around the virus eventually impacted the tourism and retail sectors, and weighed on sentiments around global growth, leading to selloffs in the latter part of the month.

Fears around a slowdown in global growth directly impacted oil prices, with the Brent oil price erasing its Dec ’19 gains while it heads lower towards a near term support of $50. Inversely, Gold climbed further to reach highs of $1,611 per ounce before stabilising between $1,580 and $1,550 amid risk-off sentiments

Global equities fell, ultimately dragged lower by Asian equities which bore the brunt of the coronavirus selloff. In fact, the month ended with most major equity indices in the red YTD, with only Nasdaq remaining positive. However, the tapering of concerns around the virus in the first week of Feb saw US equities continue to outperform other regions and eventually went back on track to notch fresh all-time highs.

The risk-off sentiment throughout January also helped support Fixed Income (FI) as demand for sovereign debt, notably US Treasuries (UST), increased. This led to the UST 10Y yield falling to key support of c. 1.50% at the end of the month before rebounding in the first week of Feb. Fund flows into higher quality bond ETFs also dominated this month as markets took risk off amid concerns that the virus will impact corporate earnings.

The risk-off sentiment also led to increased volatility in the FX market and saw the USD strengthen considerably, with the DXY climbing to 98.50 in the year to 6th Feb – its highest in four months. On top of concerns around the coronavirus, GBP also weakened last week amid potential UK-EU trade complications after Johnson and Barnier clashed over rules around post-Brexit trade arrangements.

OUTLOOK

We would simply ascribe a one-third chance it gets much worse with infections climbing until Q2 having a much greater impact on GDP growth in China, Asia ex-Japan and even globally; one-third chance markets are pricing in virus where we are now, i.e. nasty but only having a short-term; one-third chance we see infection rate stabilise and peak in Feb, thus allowing a further risk rally.

There is danger markets get too optimistic too soon. However, China’s unilateral decision to halve trade tariffs is clearly positive, especially if Trump responds graciously. There is no doubt the virus is Xi Jinping’s biggest challenge since taking over in ’12 and he has no one else to blame. He, and the Communist Party of China (CCP), have suffered an enormous blow to their prestige, competence and the China ‘model’.

The only way he, and CCP, can respond is to throw everything they can at containing this virus and to more aggressively reflate the Chinese economy. By jettisoning trade tariffs, Xi is putting the economy ahead of principle. This is positive for the economy and for equities and reduces risk.

Elsewhere, S&P 500 companies’ earnings reports in Q4 are beating consensus forecasts handily whilst recent macroeconomic data in the US is positive, as is a robust ADP report. These are fundamentally important for risk assets. Whilst we should be cautious in the short-term now equities have rebounded strongly with US equities at fresh all-time highs, the medium- to long-term case that there is no alternative (TINA) to equities remains in place.

![]()

![]()

![]()

![]() EQUITIES

EQUITIES

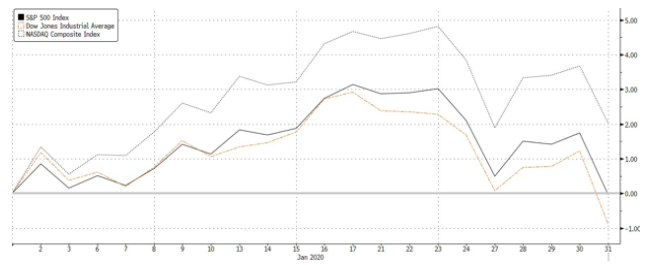

The S&P 500 (-0.16%) lost most of its mid-month gains to close the month mostly flat (Figure 1), while DJIA (-0.99%) performed likewise, weighed lower by a steep decline in Boeing. Nasdaq (+1.99%) managed to hold on to some gains, with tech stocks again outperforming on the back of several earnings beats from the likes of big hitters such as IBM and Facebook.

Figure 1: US major indices’ returns in Jan ’20. Source: Bloomberg

The risk-off appetite from investors saw moves out of Materials, Financials, and Healthcare, while Utilities outperformed alongside IT, which remained surprisingly resilient despite the run-up it had already seen. Energy underperformed significantly, though understandably so as oil prices likewise came sharply off Jan highs (Figure 2).

![]() Figure 2: S&P 500 sector returns in Jan ’20. Source: Bloomberg

Figure 2: S&P 500 sector returns in Jan ’20. Source: Bloomberg

Macroeconomic data was generally supportive in Dec, with ISM Manufacturing PMI rebounding sharply in Jan to 50.9 (vs est. 48.5), while CPI rose 2.3% YoY (vs est. 2.4%) in Dec. Housing starts rose 16.9% MoM (vs est. 1.1%) to a 13Y high as lower mortgage rates, along with higher wages and low unemployment helped buoy demand. Overall, GDP grew at an annualized 2.1% on 4Q19 (vs est. 2.0%), the same as the prior period although consumer spending moderated, and business investment continued to deteriorate. Notably, NFP also fell short of expectations, rising +145k in December (vs. est. +160k) although this came after a strong print in November.

Earnings season is also ongoing, with close to half of all S&P 500 companies having reported as of 31st Jan. Of the 45% that did, 69% reported a positive EPS surprise, while close to two-thirds reported a positive revenue surprise. The current estimated earnings decline in 4Q19 sits at roughly -0.3%, while estimates sit closer to -1.6%.

Shares in Europe were likewise down across the board (Figure 3), with shares in the UK leading losses, while the French CAC 40 trailed behind. In terms of data, German manufacturing PMI in Jan rose to 45.2 (vs est. 44.5), while the overall Eurozone figure came in at 47.9 (vs est. 47.8) compared to 46.3 a month earlier. The move, despite it still being a contraction, is its strongest reading since April 2019. Separately, ECB’s chief economist expressed his view that rising labour costs would eventually re-ignite inflation in the region, expressing confidence that the ECB was on track toward its inflation goals.

Figure 3: European major indices return in Jan ’20. Source: Bloomberg

Utilities outperformed significantly, no doubt a result of a risk-off move into defensives, while Basic Resources and Oil & Gas were key laggards. Autos underperformed significantly amidst renewed fears that Trump would impose stricter tariffs on European carmakers (Figure 4).

Figure 4: Stoxx 600 sector returns in Jan ’20. Source: Bloomberg

Asian markets bore the brunt of the selloff, with the MSCI Asia ex-Japan Index (-5.16%) logging steep declines, while the SHASHR (-2.41%) and HSI (-6.66%) were still on their Chinese New Year holiday. Nikkei (-1.91%) also closed lower, while MSCI ASEAN (-5.16%) underperformed the broader region.

In Asia, equity markets were undoubtedly alleviated earlier in the month by the news over trade – China understandably one of the top gainers in the region. HSI also rallied, in part off the back of this news, but also as tension on the streets appeared to have tapered off toward the holiday season. Overall, the MSCI Asia ex-Japan gained, while Japan and Sensex lagged the broader region. This was however quickly erased following the outbreak of the coronavirus.

New data also showed China’s GDP grew +6.1% in ‘19, down from +6.6% a year earlier to its slowest pace in 29Y. The results were, however, largely in-line with economists’ expectations and the government’s target of 6% to 6.5%. Industrial output grew 6.9% in ‘19 (vs est. 5.9%) while FAI picked up for the 1st time since June to grow 5.4% in ’19 (vs est. 5.2%), signaling a firmer recovery could be underway.

FIXED INCOME

Figure 5: FI sector returns in Jan ’20 Source: Bloomberg

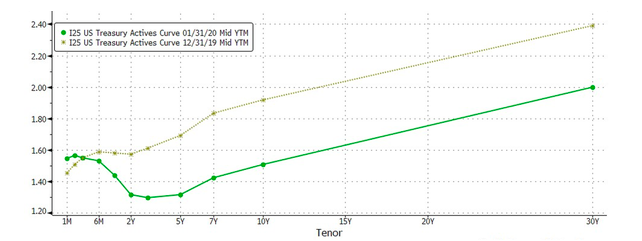

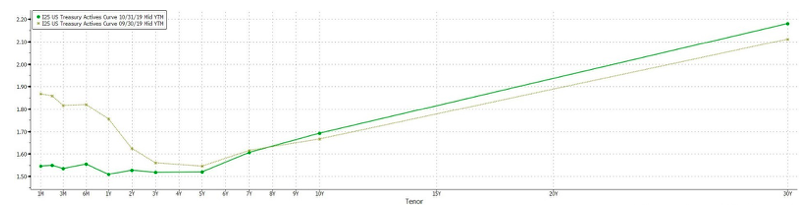

Fixed income markets were risk-off as well as we saw rotation into higher-quality debt. Flows moved back into sovereign debt, with USTs outperforming all other sectors in the asset class (Figure 5). Prices rose and yields fell across the UST curve, with the 10Y yield falling to a support at c. 1.50%. This led to duration spreads flattening (Figure 6), with the 3m/10y inverting momentarily towards the end of Jan, reviving memories of growth fears seen last year.

Figure 6: UST yield curve comparison between Dec’19 and Jan ’20. Source: Bloomberg

The FOMC also had its first meeting of the year and kept its key interest rate unchanged while indicating that monetary policy will stay on hold. Markets expected this and had little reaction to the news. However, the FOMC raised the IOER and overnight repo rates by 5bps each to 1.6% and 1.5% respectively and said it would continue expanding its balance sheet into 2Q20. It also tweaked its language to say that current monetary policy is appropriate to support inflation “returning” to the 2% target, from saying prices were “near” the goal. Powell clarified in his post-meeting comments that the new language was meant to clarify that the central bank is “not comfortable with inflation running persistently below” the 2% goal.

Looking at other parts of the world, JP Morgan estimates that the net supply of euro-area sovereign bonds this year will amount to EUR 188bn, the lowest since ’08. This comes against a backdrop of lower borrowing costs and is lower than the EUR 240bn ECB pledged to buy under its bond-buying program. The expected slowdown in issuance of sovereign debt in the region saw auctions in Spain and Italy during the month draw record demand.

Global credit spreads all widened too, though a fall in sovereign yields helped cushion the impact. US HY spreads widened the most to reverse the narrowing seen in Dec (Figure 7) as concerns around the coronavirus, and its potential impact on the economy and corporate earnings led investors to pull funds out of the sector. UBS noted that the concerns around the virus led to $2.2bn worth of outflows from bond funds since 24th Jan. Global HY issuance was also strong up till the last week of the month. Data from Dealogic showed that global HY bond issuance in Jan amounted to $73.6bn, exceeding any other monthly total over the past 25 years.

Figure 7: Credit spreads widen to reverse Dec’ tightening. Source: Bloomberg

Elsewhere, JP Morgan credit analysts have lowered forecasts for US HY returns, spreads and yields for ‘20 following a strong rally for the debt in Dec. It slashed its return outlook to 6% from 7.5% initially seen in late Nov. YE20 yield forecast was also cut to 6% from 6.25% and spreads to 425 basis points over Treasuries from 440bps. This does not change our preference for riskier debt over IG as valuations in the latter remain rich. However, given the late-cycle environment, we are in, we continue to advise investors to remain cautious when dealing with the riskier end of the credit quality curve.

Concerns around the virus also affected primary issuances in AXJ. Prior to the escalation of the illness, sales of Asia dollar bonds rose to $42.5bn in Jan – a record for issuance levels in any Jan. However, the virus, coupled with the Lunar New Year holidays, saw issuance come to a standstill in the last two weeks of Jan. Despite this, we remain positive on AXJ FI. On top of the reasons highlighted last month – reflation in Asian economies; positive technicals – we remain of the view that central banks in Asia have the willingness, and the ability, to cut rates still. Apart from wanting to support their economies amid the viral outbreak, central banks will undoubtedly move to cut rates to prevent their currencies from strengthening too much as the hunt for yield brings fund flows into the region.

FX

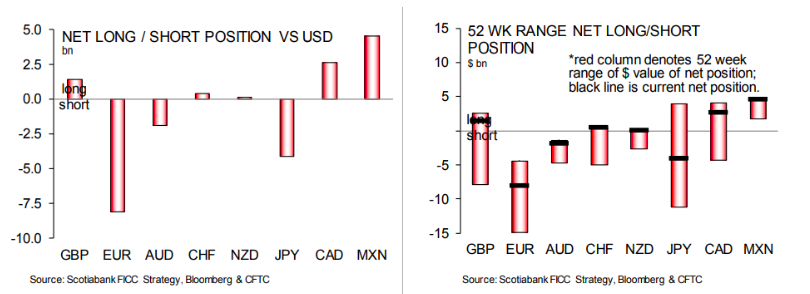

Concerns around the coronavirus saw USDCNH break above 7 again momentarily and caused a spike in volatility in the rest of the world. As for the rest of Asia, investors began to assume the worst; tourist and export-based economies such as Australia (AUD -3.74%), Thailand (THB -3.69%), S. Korea (KRW -2.86%) and Singapore (SGD -2.86%) were affected the most YTD (6th February).

The relative outperformers YTD in Asian FX were IDR (+1.67%), INR (+0.26%), PHP (-0.24%) and VND (-0.20%) as investors favoured higher-yielding FX and as oil prices fell. In the G7 space, JPY experienced a healthy bout of volatility as traders rode the 107 to 110 range as shown by positions as uncertainty rocked markets (Figure 8).

The remainder of the G7 currencies also weakened as the ultimate haven, the dollar, supported by the resilient consumer, once again led the charge. The DXY climbed from 96.40 to 98.50 YTD (6th February). GBP and EUR also led losses (aside from AUD) as traders unwound longs (GBP) and remained bearish (EUR).

In the coming months, aside from an overall slowdown/weakness in FX, we continue to see further weakness in the AUD, THB, KRW, and SGD as the economic damage from the coronavirus seeps its way into trade-related data and of course, tourism.

However, the damage is reparable. Countries affected by the coronavirus have reacted much quicker to contain, mitigate and attempt to treat the virus. Although we understand the asymptomatic attribute may drive fear, we do not believe this fear will last forever. China, much different than it was in ‘03, is much more capable in stabilizing and stimulating its economy using state-owned entities. Like we have seen for the second time on 31st Dec, the RRR rate was cut once again and as we write this, China has ordered state-owned funds, lenders as well as brokerages to pump liquidity to virally affected parts of its economy.

Figure 8: Long/Short Positions against US.

COMMODITIES

The Brent oil price experienced a tumultuous start to the year as it fell from its high of $71/bbl (from Iran-US tensions from the death of Iranian General Soleimani and the signing of Phase One of the trade deal) before ultimately falling amid fears of a global slowdown from the coronavirus. This prompted a rapid unwinding of long positions that caused Brent to reverse all its gains from Dec ‘19 (Figure 9).

Inversely, Gold climbed further to reach highs of $1,611 per ounce before stabilising between $1,580 and $1,550.

We believe that the virus will continue to take center stage for commodities and metals as the demand for energy falls, particularly due to the slowdown of auto-manufacturing economies in Asia. This will, in turn, lead to a build-up in inventories as we believe demand growth will slow for the better part of ‘20.

We see further room for Brent to fall before finding support at the $50 region due to three reasons – a recent OPEC+ emergency meeting was called for (OPEC+ officials recommended 600kbpd of additional cuts in output, but Saudi Arabia and Russia are at odds around this decision); positioning still places investors net-long and therefore more room for a sell-off; the coronavirus’ pressure on China might hamper its growth in the short-term and affect near-term demand (some Chinese commodity companies are reportedly claiming force majeure on some of their contracts).

Although concerns of the coronavirus infection rate will continue to weigh down on oil, we believe OPEC+ policy revisions and a slowdown in fears (as markets tend to do) will place a floor on the oil price within the coming month.

Figure 9: Chart showing WTI Oil vs Net Positions.

Jan 15, 2020 | Articles, Global Markets Update

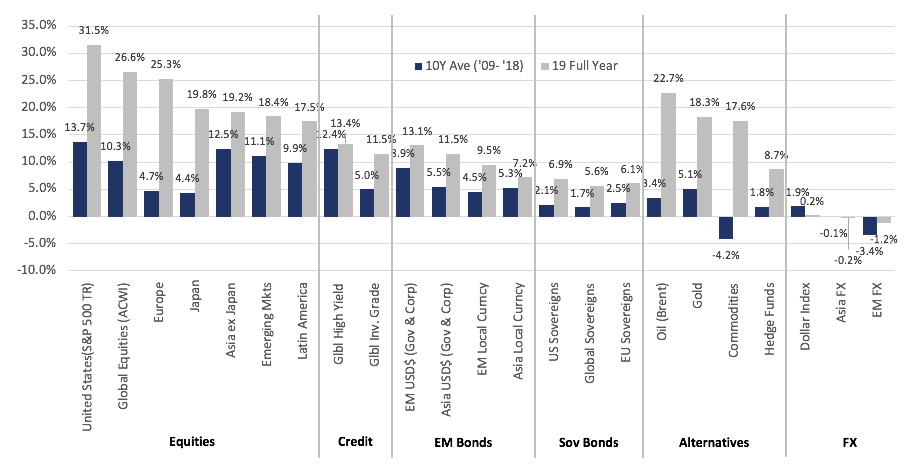

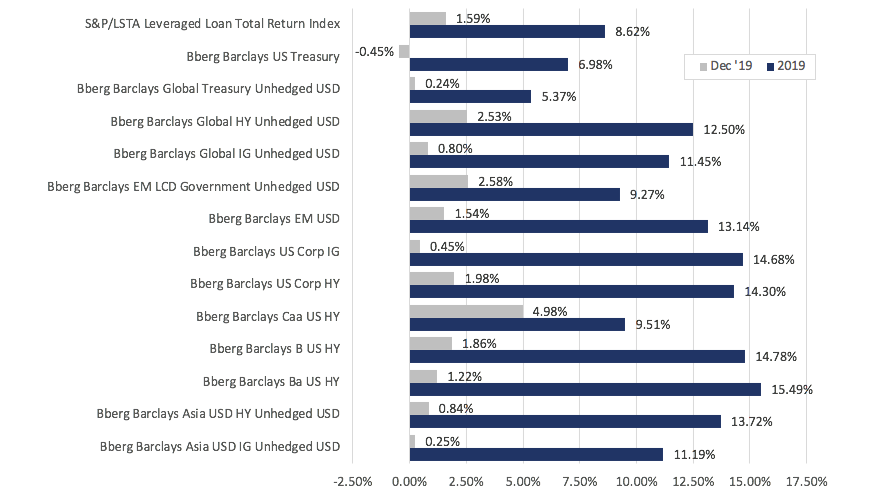

All asset classes had an extraordinary year in ’19 with most far surpassing their 10-year averages (Figure 1). Geopolitical uncertainty saw various asset classes move sideways for almost the first half of the year, but markets picked up once we saw clarity.

Equities were easily the best performing asset class with US indices leading the charge to close the year at new all-time highs. Gains in the asset class were driven largely by expansion in multiples – more so in the US than in any other region – making equities more expensive in absolute terms. Fixed income also saw robust gains across the board as investors hunt for yield. This year saw negative-yielding debt reach $17tn at its peak, pushing investors either further down the duration curve or towards lower quality credit, thus allowing global high yield (HY) to outperform the other FI sectors.

Gold had its best year since ‘13 and rose to a new 6Y-high as investors, especially in Q4CY19, embraced its merits as a safe haven asset and portfolio diversifier. ‘19 was a year of record low FX volatility with DXY up just 22bps as USD sold off against rest of world (ROW) FX in Q4 having been up c. 2.5% at the end of Q3CY19. Oil also rose strongly for its best year since ‘14 – again much of the gains seen in Q4CY19 after OPEC cut production further and then SAUDI ARABIA additionally cut more.

Fig 1: Global multi-asset total returns. Source: LGT, Bloomberg

OUTLOOK

We are risk-on as we start the new year. While we are still bullish on equities, we see relatively less value in US equities having seen its performance last year. The expansion in multiples of that magnitude in the US will eventually need to be supported by earnings growth. However, we think that the probability of that happening is low given the US is late-cycle with regards to expansion and faces a slower economy this year on a YoY basis relative to others which might be stable, or even better (EMs especially). A number of people see US equities underperform equities in ROW in ‘20 given potentially relatively weaker earnings per share (EPS) growth of c. 5% in FY20 relative to the 10%+ for ROW.

In addition, US equities also face potential political/regulatory headwinds – some of which have bipartisan support – and higher barriers to monetary/fiscal policy action bar a material slowdown. This compares with economies in other parts of the world that has more capacity for further monetary easing or fiscal reflation (which we already saw in Japan and might potentially see in Europe).

However, we see relatively less value in FI and are underweight the asset class. We do not see anything in the near-term that will cause a blow-up in the space but acknowledge that there are greater risks here compared to equities – there is the possibility of ‘fallen angels’ in BBBs; defaults in leveraged loans. Moody’s also argued that US HY FI is overvalued with unattractive risk-reward compensation given how spreads have tightened considerably in’19.

Within the FX markets, there are strategists arguing for USD relative weakness – notably against emerging markets (EM) currencies/JPY. Whilst we can see risks for USD in ’20 – important as a driver of portfolio flows to ROW equities and EM equities more so – equally, we’d want to see a clear trend of USD weakness develop before being too bearish. We struggle to be too negative on it as opposed to other developed markets (DM) FX. Gold has merit as a ‘safe haven’ diversifier in a way overvalued sovereign FI is no longer. Oil has upside if one agrees on US shale oil production. Goldman Sachs (GS) forecasts that growth in shale inventory will slow sharply given firm demand from EMs, OPEC’s disciplined production and IMO regulatory action. In addition, oil remains a warrant against the Middle East geopolitical flare-ups, not unlike what we saw happen between the US and Iran last week.

A US airstrike killed Qasem Soleimani, a top Iranian commander, thus explicitly raising the temperature and shifts the scenario from being a proxy war to a direct confrontation. Much now depends on Iran’s threatened retaliation which the US has stated will result in a 2nd round of US attacks on Iranian targets. This, thus, has scope to escalate – the key question is to what degree. We don’t think it is in Iran’s interest to escalate this to a full-on military conflict (as much as it is not in the US’s interest), but it cannot sit back and do nothing. This creates uncertainty and will likely drive oil prices.

We have warned previously that Trump might behave more erratically around impeachment pressures and this deliberate attack follows the same playbook Clinton used. That impeachment process now appears it will be dragged out as opposed to hopes (for markets at least) that there will be a quick Senate trial. This is not good news for certainty and for further risk of erratic behaviour – to the degree the US-China trade deal is not yet signed – to hurt risk-on assets.

As ever we continue to strongly argue that we are in a low return, high volatility set of market conditions – a strategic view that was borne out in ’18 but clearly failed last year – that requires us to be diversified as much as possible and seek uncorrelated alternative income strategies. On the evidence, the USD might ease-off, it may be appropriate to run with less USD-hedged allocations too. Capital market assumptions forecasts for the next five years suggest higher quality FI could deliver zero returns (with capital losses offset by coupons) while equities offer 5-6% with the S&P 500 closer to 3% (EM FI and equities offer highest returns but obviously at higher volatilities). These implied returns are not compelling and make capital preservation even more important when returns are low. After equities had a banner yearning ’19, we need to be quick to react to any major correction.

![]()

![]()

![]()

![]() EQUITIES

EQUITIES

Global equities were broadly higher following Trump’s sign off on a ‘Phase One’ trade deal with China, notably so in the US where markets dismissed impeachment news as all three major indices pushed deeper into the all-time high territory. The S&P 500 gained +2.86% in December, taking ‘19’s total return to an impressive +31.48%. Likewise, the Dow and Nasdaq gained +1.74% and +3.54% respectively this month, with the latter outperforming the year with a +36.74% total return as tech stocks led the advance (Figure 2).

Fig 2: US equity indices total returns. Source: Bloomberg

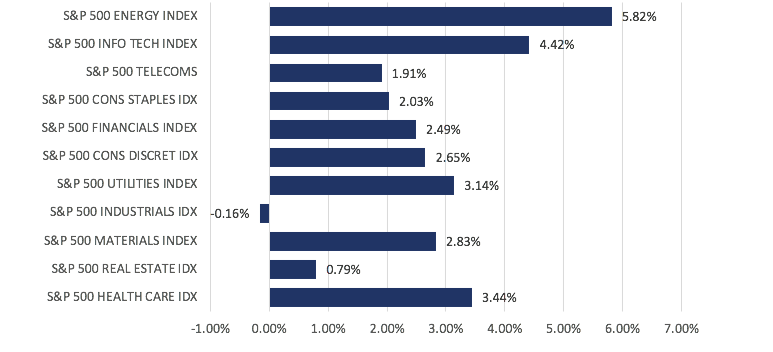

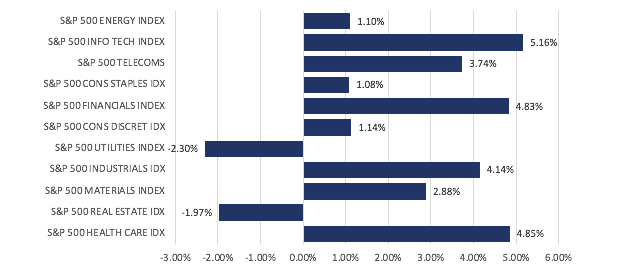

The S&P 500 saw a broad-based gain this month, with all sectors seeing a positive close. Gains were led by Energy and IT stocks, though interestingly the two were the worst and best-performing sectors this year at +48.04% and +7.64% respectively (Figure 3).

![]() Fig 3: S&P 500 sector returns in Dec. Source: Bloomberg

Fig 3: S&P 500 sector returns in Dec. Source: Bloomberg

Markets in the US were also supported by generally positive data prints, with Q3 GDP matching expectations at 2.1%, while core PCE gained 2.1% QoQ for the same quarter. University of Michigan’s consumer sentiment index also had a slight beat, coming in at 99.3 (vs est. 99.2). November’s Non-farm payroll print came in surprisingly strong at +266k (vs est. +183k), even if one were to subtract the 48k GM workers that returned from strike. Unemployment fell to a 50Y low of 3.5%, while wage growth stood at +3.1% (vs est. 3%). The only weak spot came in US retail sales, which gained only +0.2% MoM (vs est. +0.5%), although October’s reading was revised up to +0.4% from the previously reported +0.3%.

Over in Europe, the ECB left rates unchanged as expected, re-affirming commitments to its bond-buying program and low rates until the region can get closer to its inflation goal. Overall, conditions were generally helpful, allowing the Stoxx 600 index to gain 2.06% for the month, taking the full-year gain to +25.26%. Unlike last month, shares in the FTSE 100 outperformed at +2.67% this time around, while DAX lagged behind with a meager +0.10%, after Germany’s manufacturing PMI fell unexpectedly to 43.4 in December (vs est. 44.6) (Figure 4).

Fig 4: European regional indices Dec total returns. Source: Bloomberg

In Asia, equity markets were undoubtedly alleviated by the news over trade, with China understandably one of the top gainers in the region, gaining 6.20%. The HSI also rallied +7.00%, in part off the back of this news, but also as tension on the streets appeared to have tapered off toward the holiday season. Overall, the MSCI Asia ex-Japan (AXJ) gained 6.42%, while Japan and the Sensex lagged the broader region at +1.56% and +1.16% MoM respectively.

There were some encouraging numbers out of China that showed stabilization and a pickup in growth momentum. We also saw China unveil more pro-growth measures, with financial institutions now required to price floating-rate loans on the back of the revamped LPR as of 1st Jan, which will lower costs for c. CNY 152tn worth of outstanding loans in the market. The revised securities law also simplifies the process for corporate bond issuance and raised the penalty for issuance fraud to CNY 20m from CNY 600k, which will take effect on the 1st March.

FIXED INCOME

Fig 5: FI sector returns in Dec and in 2019. Source: Bloomberg

The fixed income market was positive in Dec (Figure 5), leading various sectors to see multi-year high YoY returns. Global investment grade (IG) and HY saw their best YoY performance since ’09 and ’16 respectively, while US Treasuries (UST), the only sector to fall in Dec, saw its best YoY returns since ’11.

Global IG spreads narrowed in the last few days of ’19, ending the year at 94bps – 59bps tighter YoY while global HY spreads narrowed 127bps to 419bps. Credit spreads ended the year near/at ’19 lows (Figure 6) as central banks around the world adopted, in one way or another, monetary easing policies. Apparent progress in US-China trade negotiations and more geopolitical certainty also contributed to the risk-on sentiment, thus supporting HY debt.

Moving forward, the tight spreads are attracting primary issuance of c. $120bn in Jan after pausing for much of Dec. HY could also see a busy month as companies look to refinance debt, with c. $9.5bn worth of HY bonds scheduled to mature or be called this month.

Fig 6: Corporate credit spreads in 2019. Source: Bloomberg

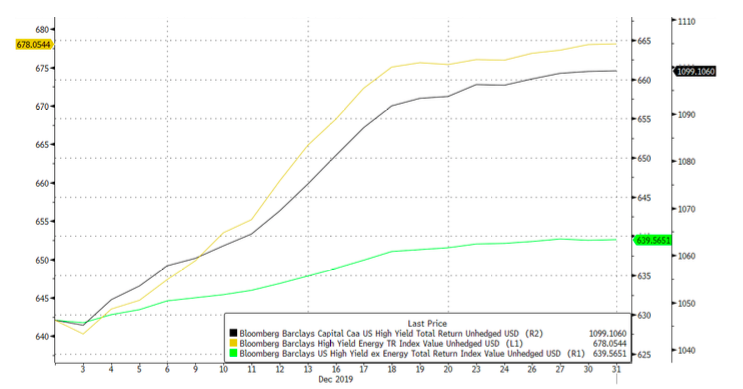

Within HY, CCC debt ended the month as the best performing sector within FI. With spreads rising above 10% for the first time since ’16 after being sold off earlier in the year, coupled with improving market risk sentiment, yield-hungry investors jumped at the chance after hiding out in the BB space for much of ’19. Energy led gains in the sector with oil prices rising for most of the month (Figure 7).

Fig 7: Returns of HY Energy debts vs CCC and HY ex-energy. Source: Bloomberg

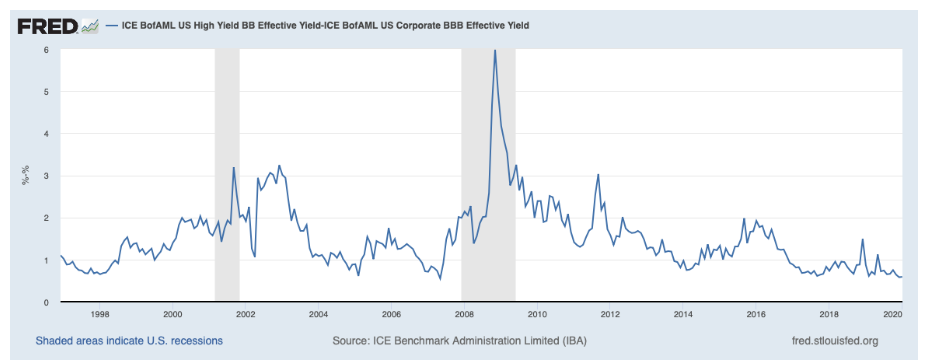

This hunt for yield also saw spreads between IG and HY narrow. In particular, ICE BofAML data showed BB/BBB spreads to be at its lowest since pre-GFC (Figure 8), suggesting how overvalued the BB space has become. This trend is likely the reason why Wall Street analysts are forecasting gains of only 1% – 7.5% for US HY in ’20.

However, not all analysts share this view – Blackrock raised its rating for global HY to overweight, arguing that the sector will be supported by stable monetary policy worldwide, and the potential for an inflection in growth.

Blackrock also simultaneously downgraded global IG citing rich valuations, especially with negative rates in Europe and Japan.

Fig 8: BBB/BB spreads. Source: Bloomberg

Blackrock also upgraded EM local currency debt (LCD) to a “high conviction overweight” noting the attractive coupons and the potential for currency appreciation as USD sees a potentially trying year in ’20. EM LCD saw a strong Dec as USD weakened.

Within EM, we continue to see value in AXJ FI, particularly in the HY space. Apart from a potential reflation in the Asian economies, the sector is likely also supported by technicals. Many HY issuers advanced their refinancing to ’19 and hence these volumes are unlikely to be sustained in ’20, providing support for prices. While China saw another record year of onshore corporate defaults, we see little reason for concern. A number of defaults are a result of idiosyncratic reasons and are not representative of the entire market. Besides, the amount of onshore defaults (c. CNY 130bn in the last few weeks of ’19) is small relative to the entire market.

Finally, we see an additional source of risk in European companies. Moody’s expect companies in Europe to face more rating cuts and higher odds of default this year. It expects defaults to almost triple as more HY companies struggle with weak demand. Moody’s also forecasts the rate of missed payments in the region to catch up with the USA.

FX

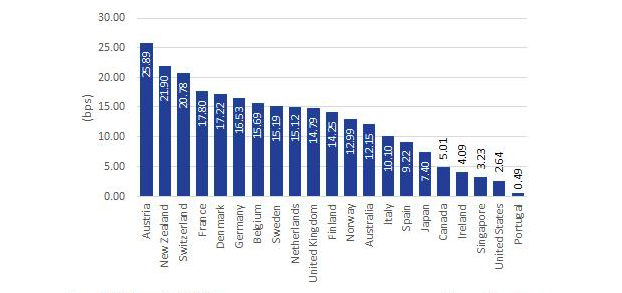

USD was by far one of the worst-performing currencies in Dec, weakening against all of its G10 peers and most of the EM currencies. DXY fell 1.92% over the month, falling below 97 for the first time since July ’19 while the JPM EMCI gained 2.66%, its best month since Jan ’19. FX movements continue to be driven by geopolitical events like Brexit and US-China trade over the month. The dollar recovered slightly on the back of positive economic data but failed to sustain the momentum. The weakening sentiment for the USD was reflected in the extended fall in aggregate long USD positioning while GBP positioning turned marginally net positive for the first time in ’19 (Figure 9).

Fig 9: USD and GBP positioning as at 24 Dec ’19. Source: Bloomberg

The Dec weakness for DXY led the index to end ‘19 just 22bps higher while CAD ended the year as the best performer within the G10 group. Asian currencies saw a good year too, with most currencies stronger against the dollar, led by THB. However, tensions and protests in larger European and LatAm EM markets, particularly in Turkey and Chile, weighed on the JPM EMCI, which ended the year -1.36%. Volatility in FX markets also spiked up in the first week of ’20 following US’s assassination of Qasem Soleimani with haven currencies strengthening.

Looking forward, we continue to remain a USD bull until proven otherwise. Despite recent events, USD has proven to be very resilient since the global financial crisis and remains to us the least bad major DM currency fundamentally. However, we are more cautious on USD this year than in the previous five years as US GDP might slow relative to its peers while the S&P 500 looks relatively unattractive. Swaps around fully hedged FI is also not supportive of FIIs buying hedged USTs despite the relative real yield differential positives. If FIIs anticipate a weaker USD, this will boost hedging demand or reduce unhedged buying. Lastly, fiscal reflation looks improbable in the USA this year but more likely to happen in Europe, Japan and ROW – fiscal spending helps strengthen currencies where this happens. In addition, a key catalyst for EUR gains would be signs that Germany is closer to abandoning its overly prudent ‘zero budget’ policy that’s become institutionalized.

Fig 10: FX returns in 2019. Source: Bloomberg

COMMODITIES

The Brent oil price extended its uptrend in Dec after an initial tumble in the first week of the month, resulting in its best year since ’14. Much of the gain here was on the back of an OPEC production cut, with Saudi Arabia committing larger than required cuts. Gold also had its best year since ‘13 and rose to a new 6Y-high at $1,550/Oz as investors, especially in Q4CY19, embraced its merits as a safe haven asset and portfolio diversifier.

Brent oil rallied in the first few days of January following the assassination of Soleimani, but it was surprising that it failed to break above its resistance at $70 until today (08 Jan 2020). This suggests that either markets doubt a severe Iranian response or that oil fundamentals are looking ‘softer’. Oil is still technically in the range of $55-75/brl with low $80s an even bigger resistance. Bears continue to point to an expected surplus of production and building inventories as reasons to be wary of upside from here. However, the fact is Iran probably has the military capability and proximity to close Hormuz Straits through which 40%+ of the world’s sea-bourne oil exports travel.

Dec 12, 2019 | Articles, Global Markets Update

Markets traded mostly higher in November on the back of improving trade headlines and despite Trump’s signing of the Hong Kong Human Rights and Democracy Act and potential sanctions against Chinese officials for abuse against the Uighur Muslims. We saw indices in the US push all-time highs, while the Stoxx 600 also came within 1% of their all-time highs during the month. While Asian equities saw more of a mixed performance amid the protests in Hong Kong and weakness in Chinese economic data, global equities were buoyed by positives – particularly in the US and Europe. This aligns well with our view (and Morgan Stanley’s), which is an expected recovery in the global economy from 1Q19, led by Emerging Markets (EM) given the easing of trade tensions and scope for easier monetary policies in the region, while Goldman Sachs expects the US economy to also pick up as the effects of lower interest rates start to kick in.

Corporate credit – in particular, High yield (HY) debt – was a key beneficiary of this month’s risk-on appetite, with investors chasing yields and rotating out of sovereign debt, driving yields, more broadly, in the Investment Grade (IG) universe higher as well. We also saw some steepening in the US Treasury (UST) curve, after the Fed held rates steady and indicated that it will continue to do so unless something dire happened which would impact the US economy. We also saw safe-haven currencies weaken, with the exception of the dollar which gained in the back of stronger data, as did the EUR while GBP continued to ebb and flow with the latest news reports on the UK elections. Currencies in Latin America underperformed and suffered amid the ongoing protests in Chile, as well as the resumption of steel tariffs on Brazil and Argentina by the US later in the month.

OUTLOOK

Hong Kong equities are almost flat YTD relative to the double-digit gains in global equities, including Asia ex-Japan where Chinese equities have led the way up. The difficult question is whether this underperformance since protests began and the economic recession as a consequence, has discounted much of the plausible risks. There are, arguably, three scenarios being a) a Chinese crackdown that would ultimately end Hong Kong’s separate system and unique appeal overnight, which would see Hong Kong equities fall sharply and struggle to recover; b) a compromise in which case Hong Kong equities would soar; c) a continued stalemate, marked by episodic spikes in violence, that the city slowly gets used to, and ultimately the protests lose ground to the realities of jobs and studies while the people move on. This might take time like the leftist riots in 1967 which lasted from May until December with huge casualty numbers after violence flared in July with bombs going off. Hong Kong has a long history of existential challenges be it the WW2 Japanese occupation and then the handover in 1997; serious riots in 1956 between pro-Chinese Communist Party and pro-Kuomintang factions that required troops to control it; 1966 riots over a hike in Star Ferry prices, 1967 riots between leftists and the British – again troops were needed; a police riot against anti-corruption reforms in 1977 and 1981; a march in 2002 against a proposed national security law; 2014 protests over Chinese proposed democracy reforms that lasted 79 days and finally 2015 riots in Mong Kok.

Interestingly an inquiry commissioned by then-governor David Trench suggested that the events had also exposed a gap between the colonial government and the people – a gap that would be “a continual danger and anxiety for any form of administration.” It highlighted the problems faced by Hong Kong’s youth, saying: “The evidence before us points to the probability that young people are less likely to put up with conditions which their parents accepted without comment.” It said solutions depended on the continuing prosperity and success of Hong Kong “since its future well-being is in the hands of the young people of today” and that it was in the youth “that Hong Kong must make its major and most significant investment.” The riots in 1956, 1966, 1967, 2014 and the current protests today had deep roots in terms of poverty, lack of opportunities for the younger people and inadequate housing. In terms of the 1967 severe riots and the 2014 and 2019 protests, the sovereign power was a clear target. The British government responded with measures to address social grievances and address the housing shortage, yet it never offered democracy or accountability. This might be one way out of the current impasse and, so far, these protests are not of the length, or violence, of 1956. Hong Kong recovered from its pasts tests and should the Hong Kong/Chinese government heed some of those earlier lessons, there is a path forward.

History would suggest, should common sense prevail by the Hong Kong and Chinese governments, as well as protesters’ use of violence, Hong Kong will survive this latest test and continue to prosper given its separate system and its unique set of skills, position, and importance. We have heard arguments Hong Kong is no longer important to China, that it is only 2-3% of China’s GDP and that the Chinese government would be happy to see a colonial-era creation become a backwater. This is inaccurate. Hong Kong raised the bulk of Chinese corporates’ offshore capital – a role even more important given the US’s veiled threats to close its capital markets to Chinese companies (as it did to Russian companies). China will retain its capital controls for many more years, making Hong Kong’s role as the key offshore intermediary critical, thus making no sense for China to allow Hong Kong to wither on the vine, barring extraordinary circumstance, suggesting the medium- to long-term view on Hong Kong equities ought to be positive even if, in the short-term, it looks obscure and horrifying on occasions. Other than the British imposing self-harm via Brexit, most people do not deliberately damage their country, which suggests support for protesters will decline should the Hong Kong and Chinese governments do things to address the underlying socio-economic problems and allow some greater democratic accountability of the, so far, dire Hong Kong governments under Chinese rule. A huge affordable housing program, limits on mainland migration to Hong Kong, assistance for the young in creating jobs and improved infrastructure are all well within the remit of the Hong Kong government given its huge reserves, and if this is not a sufficient crisis to justify spending, what is? If history repeats, in terms of solutions to this crisis, then Hong Kong equities are buys and become more so if short-term events result in further selloffs.

Our base case remains common sense will prevail, that the Chinese government will avoid cracking down on Hong Kong and that measures will be taken to address underlying grievances. Undoubtedly, radicals in the protesters will never accept what will be offered as it will be deemed too little but the key is to win back the 2mn+ people that marched in position to Chinese government’s misrule in Hong Kong as history shows Hong Kong people to be pragmatic and that their protests do lead to change.

![]()

![]()

![]()

![]() EQUITIES

EQUITIES

Fig 1: US indices returns. Source: Bloomberg

-

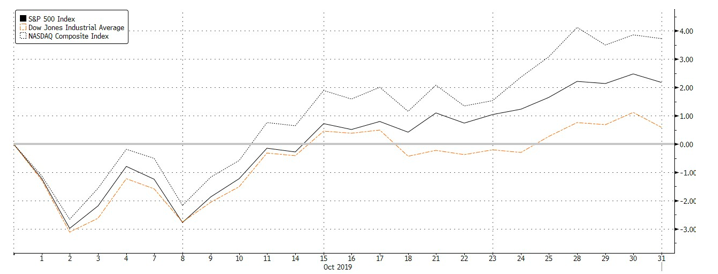

Markets in the US continued to push all-time highs in November as talks of a ‘Phase One’ trade deal – despite the concern around Trump’s signing of HK’s Human Rights and Democracy Act – added support to settlement, on top of the news that a United States-Mexico-Canada Agreement deal was nearing. The S&P 500 gained +3.40% MoM, underperforming the Dow Jones (+3.72% MoM) and Nasdaq (+4.50% MoM) (Fig 1).

-

Data, in general, continued to remain relatively positive – the University of Michigan’s Consumer Sentiment Index rose to 96.8 (vs est 95.7) in November, on top of a slight improvement in small business optimism. October’s consumer price index rose +1.8Y YoY, while the producer price index picked up a +0.4% MoM after September’s disappointing -0.4% figure.

-

3Q19 earnings season in the US has also neared a conclusion, with companies reporting a decline in earnings (-2.2%) for a third consecutive quarter. 75% of companies in the index beat EPS estimates, with Utilities reporting the highest earnings growth across all sectors at +10% QoQ. Notably, 85 companies guided for lower EPS estimates in the period ahead.

-

Ironically, despite stronger earnings Utilities, along with Real Estate, were the only detractors this month, while all other sectors were positive as Info Tech, Financials and Health Care outperformed (Fig 2).

![]() Fig 2: S&P 500 sector returns. Source: Bloomberg

Fig 2: S&P 500 sector returns. Source: Bloomberg

-

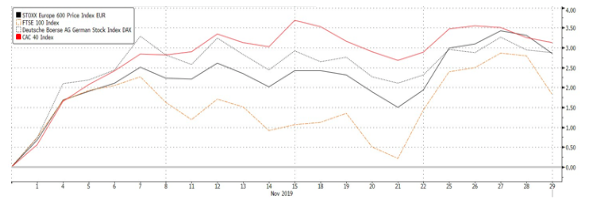

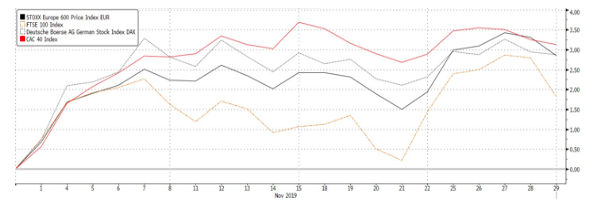

Despite the European Commission cutting their eurozone growth and inflation outlook earlier in the month, European equities were up +2.69% MoM, helped higher by the German DAX (+2.87% MoM) and French CAC40 (+3.06% MoM). The FTSE 100 (+1.35% MoM) amid political concerns ahead of the snap general elections which will be held on Dec 12th (Fig 3).

Fig 3: Returns of major European indices. Source: Bloomberg

Fig 3: Returns of major European indices. Source: Bloomberg

-

Nevertheless, data in the region was also generally positive, suggesting a bottoming in economic weakness. This was particularly so in Germany where the ZEW survey (though still negative), rose unexpectedly to -2.1 (vs est. -13.0) from October’s reading of -22.8, while the Ifo business survey improved for its third consecutive month.

-

Defensives in Europe underperformed this month, with Utilities and Telecommunications being the only sectors in the red, while Technology, Basic Resources, and Industrial Goods & Services outperforming.

Fig 4: Stoxx 600 sector returns. Source: Bloomberg

-

Based on the chart below, it was clear that returns in Asia were mixed despite the rally in both US and European equities. Nikkei and Sensex outperformed at +1.60% and +1.66% MoM respectively, while A-shares (-1.93% MoM), the HSI (-2.08% MoM) and MSCI ASEAN (-1.79% MoM) lagged severely (Fig 5).

Fig 5: Returns of major Asian indices. Source: Bloomberg

-

Exports in China fell for a third consecutive month (albeit beating estimates at -0.9% YoY vs est -3.9% YoY), while Oct industrial production weakened to +4.7% YoY (vs est. +5.4% YoY). Capital spending slowed, while retail sales growth slowed to +7.2% MoM (vs est +7.8% MoM). Industrial profits also fell 9.9% in Oct amid slowing domestic demand and trade tensions. The silver lining came in Caixin’s manufacturing PMI, which rose to 51.8 in Nov (vs est. 51.5), with output and new orders seeing some pickup.

-

To some extent, this was mitigated by the People’s Bank of China which made unexpected moves to add liquidity to the banking system by offering loans to banks and trimming its benchmark 1Y/5Y LPR by 5bps, and cuts to its short-term repo rate (for the first time in 4Y).

-

Overall, weakness in China was understandable given the poor data readings, and this, in turn, weighed on equities in the ASEAN region. Likewise, this applied to Hong Kong, although share prices in the HSI also came under heavy pressure from the ongoing protests and concerns around a decline in economic activity.

FIXED INCOME

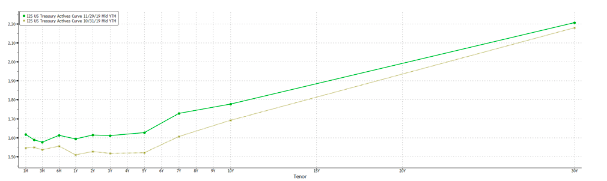

Fig 6: UST curve. Source: Bloomberg

Risk-on markets in November saw sovereign yields extending their rise throughout the month. The UST yield curve flattened slightly, and yields rose across the curve with the belly of the curve seeing the largest MoM shifts (Fig 6), resulting in a 30bps MoM fall in USTs. Reports at the start of this month showing the Fed, in its review of its monetary policy tools, considering allowing inflation to temporarily run above its 2% also helped the curve steepen, but effects from multiple trade-related headlines took over and introduced volatility in USTs, causing the MOVE index, which tracks US interest rate volatility, to shoot up (Fig 7).

Fig 7: MOVE Index shooting up in the first week of December. Source: Bloomberg

-

Corporate credit outperformed sovereign debt again this month as the hunt for yield continued to lead inflows into HY debt. US and Asia were slightly more resilient, with both IG and HY managing to register positive returns, while IG in other parts of the world fell.

-

Data over the month also seem to point towards a global growth recovery, supporting the case for HY. However, we continue to watch default risks very closely. The number of bonds in the ICE HY index trading with spreads of more than 10% – a commonly used definition for distressed debt – has risen during the month to the highest since ’16 as investors move out of lower-quality CCC debt.

-

Protests in Chile and Columbia saw the countries’ debt weigh on the EM USD-denominated debt index. However, the index managed to eke out a gain as modest gains in Russian and Turkish debt managed to offset losses seen in the Latin American countries. However, USD strength weighed on EM local currency debt, causing it to be the worst-performing sector after global treasuries.

-

We remain of the view that opportunities in the EM space, particularly in Asia, are still present. Asian central banks still have space to ease monetary policy, with several of them also expressing preparedness to do so.

FX

-

Overall, the dollar performed moderately well as recent data began to lead investors away from fears of a drastic slowdown. The 10Y and 30Y yields have found some support at 170bps and 221bps respectively, supported by shorts continuing to unwind. 10Y contracts have sold off to be at their lowest net-short position since November ’18.

-

Despite overall USD exposure remaining lower in markets since June ’19, November has seen a pickup in dollar longs, likely due to the continued sell-off in treasury bonds.

-

The EUR advanced earlier this month on short coverings as ZEW and exports reported better than expected, however YoY industrial production reported -4.30% vs. an expected -2.90%. We continue to see positioning to remain flat until we near clarification on ECB policies. Resistance still remains strong along 1.11.

-

AUD positioning was very reactive towards interest rate decisions. The decision to hold rate movements until ‘20 saw a large unwinding in shorts, resulting in a stronger AUD. Positive trade development also supported AUD further. We will likely see a build-up in shorts again on further tariff developments. AUD still remains on a downtrend with key resistances seen along 0.687.

-

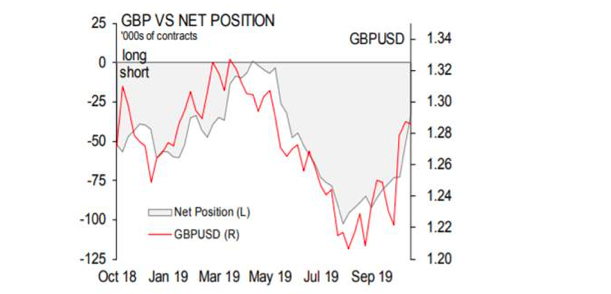

In our previous monthly, we noted that there would be an obvious increase in volatility between 1.25 and 1.35 as elections drew nearer and labeled a Corbyn victory as unlikely, simply due to the self-destructive nature of Labour policies. Johnson now leads 43% to Labour’s 32%, which implies more distance between the UK and a No-Deal. GBP remains net short with more being added in November. We expect more volatility with 1.30 to remain very supportive and are still Sterling bears in the long run.

COMMODITIES

-

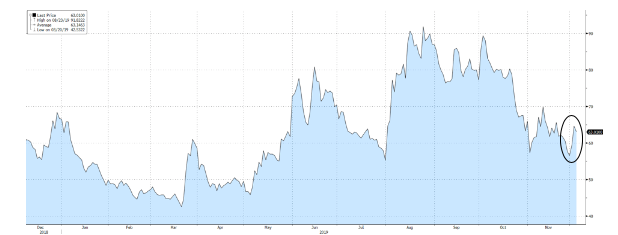

Oil and gold mainly reacted towards trade developments. Oil’s positioning has picked up since October and is now at its highest since June this year. Likewise, for Gold, positioning remains extremely net long and has in fact, risen, despite the recent sell-off during pulsated fears as Hong Kong grew larger as a wedge between China and the US.

-

Gold has fallen through technical levels and saw a prolonged period of trading between 1,550 and 1,480. We continue to believe it remains a diversifier in portfolios simply due to the prolonged acquisition from Central Banks and the ever-reliable haven attributes that it possesses in times of trade uncertainty.

- Over the month, several FOMC members also came out saying that they think US monetary policy is at a good place and reinforced last month’s meeting decision to hold rates and to continue holding rates, leading markets to price in a 0% probability of a rate cut this month.

Nov 15, 2019 | Articles, Global Markets Update

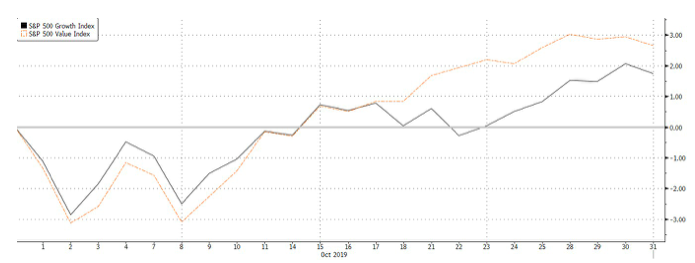

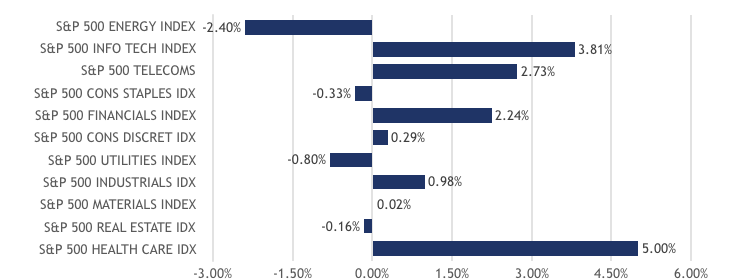

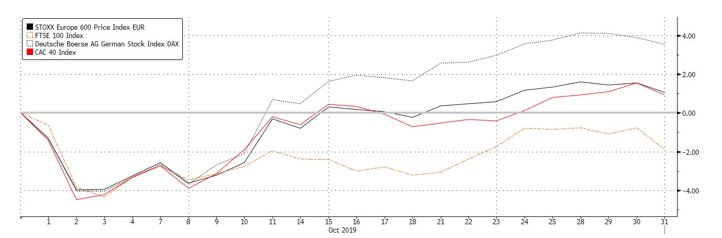

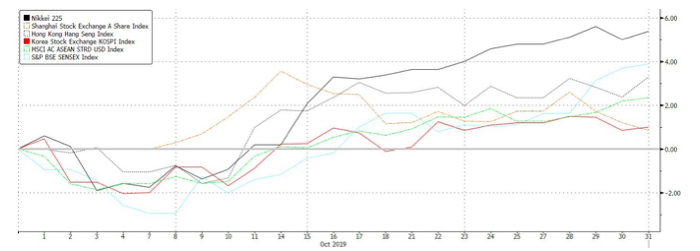

A myriad of positive factors pushed global equities higher, with the MSCI ACWI seeing a total return of 2.76% over the month, before moving higher month-to-date (MTD) in November (+1.35% MTD as at 5th November). This move higher was supported in part by the three US indices, which all achieved all-time highs. European and Asian equities also shook off earlier weakness to close higher due to improving US-China trade sentiment.

However, the improvement in the geopolitical environment helped take a degree of uncertainty off the table, leading corporate credit, particularly investment-grade (IG) debt, to outperform. Markets were risk-on throughout October, extending the gains seen in September amid a combination of a turnaround in trade negotiations, strong economic data, and better-than-expected earnings. Q3 earnings by American and European companies are beating consensus estimates handily.

The Federal Reserve again cut rates but despite the cut, they signalled that it will hold rates for the time being. The US also saw solid economic data and resilient consumption, which taken together with the rate cut, let Morgan Stanley’s model of recession odds in the next 12 months to fall back below 20%.

Volatility in foreign exchange markets remained low, with the UK Pound being the only exception. The currency saw exceptional gains in October, strengthening 5.81% against the dollar as risks of a no-deal Brexit were reduced substantially with Prime Minister Johnson’s withdrawal agreement with the EU. However, the UK parliament failed to vote through the agreement, forcing Johnson to request for an extension to the deadline. Another general election was also called, with the vote tentatively scheduled for 12th December

OUTLOOK