Apr 15, 2019 | Articles, Global Markets Update

“Ultimately lower rates are only good to a point because, eventually, the fall in rates is not just about the Fed giving equity investors a “green light” to load up on risk, but also indicates concerns around GDP growth.” `– MORGAN STANLEY

Look through or come off. Financial markets have been surprisingly resilient since the lows at Christmas Eve. Optimism over an early US-China trade deal, the obvious pivot by the Fed to be more ‘dovish’ (FI markets expect a rate cut in ’19 now) relative to its ‘hawkish’ stance last October, and other central banks’ like the ECB and PBoC and China’s more aggressive fiscal reflation, have all helped improve investor sentiment with markets rallying from very oversold conditions at YE18.

Whilst there are undeniably positive drivers, our cautious tactical stance remains as we believe the US-China trade deal will disappoint in leaving considerable post-deal uncertainties with a still material risk that a deal will fail given the wide differences between both parties over post enforcement checks. Underlying corporate earnings are still being downgraded and Q1 results may well disappoint at a time where the S&P 500 has become expensive relative to history whilst other markets are no longer cheap. GDP forecasts continue to be lowered – notably in EU – although China’s GDP outlook has ‘firmed up’.

Political risks are rising in Q2 – notably Brexit agonies, where a ‘no-deal’ is still a distinct possibility, and India, where a likely weak BJP coalition is perhaps the most likely result. Concerns remain around political risks in Turkey, Argentina, South Africa, Brazil, Venezuela, Ukraine and Thailand that could knock-on to EM FX, FI and equities. With strong rallies in equities and JY FI YTD, we believe taking some money off the table makes sense given the potential headwinds and the history of returns in most years since ’09 bar ’17’s exceptional gains. Ultimately, the rally in sovereign bonds YTD, with now around $10tn with negative yields, cannot be reconciled with the rally in riskier assets as the latter implies deflation if not a recession sooner or later.

The main risk to our cautious stance is if investors can use China’s reflation, trade optimism and central banks’ pivot to ‘bridge’ across a weak H1CY19 to an expected recovery in earnings forecast by Q4FY19 and stability in GDP forecasts that would support a further rally in risk assets (and a likely sell-off in USTs). This is not our base case, but we have put in place upside risk management triggers should we be proven wrong.

Recession or not? The inversion of the 3m/10y US yields on 22nd March, the first since ’07, may signal a recession during 2H20 based ib the past albeit this is better in telling us it will happen rather then when (it could be any time from under 12M to well over 3Y). The signal has historically been a reliable predictor of seven of the last nine recessions. There are some very plausible arguments, not least by Mr Dudley (the last New York Fed governor), that this time is different as: quantitative easing by the Fed and other central banks have lowered absolute interest levels to make it technically possible for such an inversion; the Fed is not tightening and financial conditions have eased considerably; there is a breakdown between real interest rates and underlying GDP growth since ’14 as noted by Pictet and; lastly the absence of any obvious ‘bubbles’ in financial assets or the wider economy.

In looking at the components of the US GDP, it is unlikely, given robust consumption underpinned by record low unemployment and accelerating wages (+3.5% YoY in February NFP), we will get a recession in 2020. However, the US economy will slow from Q4CY19 as Federal final spending is set to fall sharply and private sector capital expenditure is expected to ease down, making a ‘shallow’ recession quite feasible. A recession would justify the Fed’s ‘pivot’ and strengthen the FI markets view that the Fed’s next move is to cut rates.

There is a high degree of uncertainty as to what the macro data will bring from deflation and recession to inflation reigniting and GDP numbers surprising to the upside which have binary implications for portfolio construction. Our base case is we avoid a recession this year and next and that exposure to equities remains a better choice than to sovereign bonds. We will need to be nimble and tactically quick to respond to developments which includes a sizable precautionary cash holding to mitigate volatility spikes and to take advantage of them. Strategically we remain convinced we are in a 3.5-year period of low returns and that volatility will rise that argues for portfolio diversification and the use of non-traditional asset classes, as did endowment funds in recent years (Fig 1).

Fig 1: Endowment funds – asset allocation in 2007 vs 2018 Source: Bloomberg, Julius Baer

Equities

-

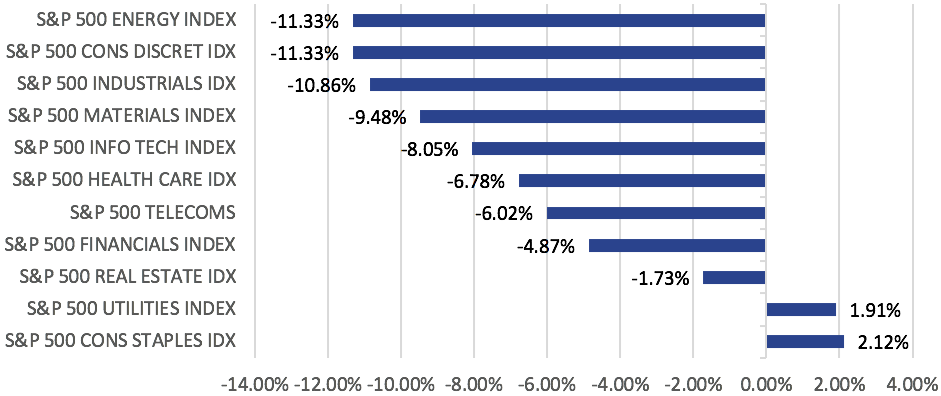

Despite a rough start earlier in the month, US equities were broadly higher as all three major indices managed a higher close in March. NASDAQ (+2.61% MoM) outperformed as Tech shares rallied, while the Dow Jones Industrial Average (+0.05% MoM) under performed after its biggest index component, Boeing, fell by as much as -17.2% from all-time highs after questions were raised over safety issues relating to the company’s 737 MAX planes. Notably, small caps also under performed, with the Russell 2,000 (-2.27% MoM) logging a decline as concerns over economic growth lingered (Fig 2).

Fig 2: March total returns of the S&P 500, DJIA, Nasdaq and Russell 2000 Source: Bloomberg

-

Technicals show the S&P 500 moved through key resistance levels to within 2% of its all-time high. We believe US equities will struggle to move higher as valuations are now expensive relative to history, and earnings are likely to contract in H1FY19 and we are trimming here.

-

Mueller’s report removes the threat of impeachment ahead of the 2020 elections and helps Trump’s re-election chances, especially if the Democrats were to choose a Socialist candidate.

-

We expect macro data to slow in 2019 as fiscal spending slows sharply in H2CY19 while private capital expenditure weakens, creating headwinds to consumption. Weaker growth would support a higher weighting in ‘growth’ sectors as IT over ‘value’. Hence, we expect Nasdaq to outperform.

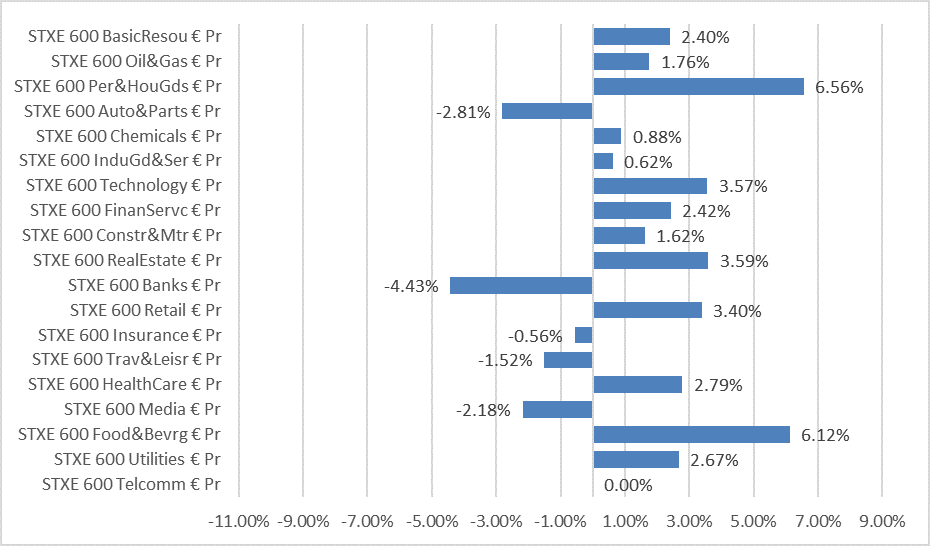

Fig 3: Stoxx 600 MoM sector performance Source: Bloomberg

-

European equities were also higher as Stoxx 600 gained 1.69% in March, led by gains in Personal & Household Goods and Food & Beverages. Bank stocks were the worst performers, after Draghi indicated rates would stay on hold for the rest of the year, a move which sent Bund yields into negative territory for the second time in history (the first being in 2016).

-

Brexit remains the overhang for Stoxx 600 and FTSE 100 and sadly, there is no agreed route and it is still a possibility of a no-deal. The next deadline is 12th April and the hope is an agreement by Parliament based on a ‘softer’ Brexit now that May is reaching out to the Labour party leader.

-

Deteriorating macro data YTD in EU could see the bloc’s economy fall into a shallower, technical recession in 2019 and may imply earnings in 2019 could contract relative to the current consensus of +4%.

-

There are political risks outside of Brexit as well. The EU election during late May might see anti-Euro populist parties gain considerable ground (even more so if the UK was to be involved in the vote) that would likely be a source of volatility in EURO and FI, which will eventually lead into Stoxx 600.

-

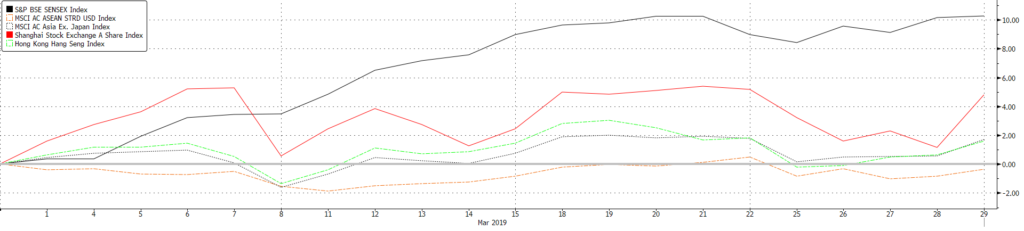

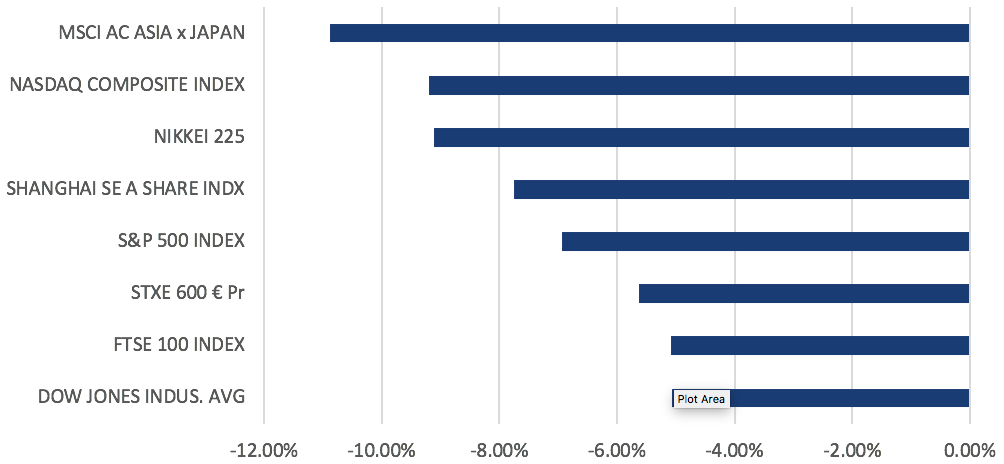

Shares in Asia also trended higher across the board, with China A-shares (+5.10% MoM) once again outperforming the region. This time, however, India’s Sensex (+7.82% MoM) surged ahead as INR also gained, taking the index to a +10.17% monthly gain on a USD-adjusted basis. For the quarter, A-shares are still significantly higher at +27.03% compared to the Sensex at +7.79% which still under performs the broader MSCI Asia ex-Japan Index which is up 11.21% in USD terms.

Fig 4: USD-adjusted Total Returns across indices in Asia Source: Bloomberg

-

-

Nikkei, on the other hand, fell 0.84% with the Yen mostly unchanged from the start of the month. Japanese equities continue to under perform in Asia, climbing +5.95% this quarter against most other indices which have logged double digit gains. Last weekend, Abe’s coalition also won approval to run a record ¥101.46tn fiscal budget in 2019, with close to ¥2tn set aside for stimulus measure aimed at cushioning the Oct 1 increase in consumption tax

-

AxJ equities are being led higher by Chinese equities and especially A-shares as local retail investors are buying again along with foreign investors, ahead of an increased weighting in MSCI EM next month. We remain overweight Chinese equities and would use any weakness to add to A-shares as we see it hitting 3,600 during 2019 as reflation of the Chinese economy comes about.

Fixed Income

-

The UST yield curve shifted lower over the month, especially in the belly of the curve with the 2Y and 10Y yields inclusive. This caused the 3m/10y spread to invert and led to the steepening of the 5y/30y spread. The Fed’s decision to hold rates in its March FOMC meeting while signalling that it won’t raise rates in ’19 caused the 10Y yield to break its 2.6% support to trade below 2.4% for the first time since December ’17. The 2Y yield also fell below the Fed funds floor of 2.25% after the meeting. However, trade optimism and strong manufacturing PMI data from US and China at the end of the month helped push yields higher. March’s developments saw USTs register their best Q1 result in 3Y as the 10Y yield fell 28bps.

-

European sovereign bond yields fell too as demand increased amid a slowdown in the European economy. The Bunds yield fell and traded below 0% for the first time since ’16. This saw the total sum of negative yielding debt represented in the Bloomberg Barclays Global Aggregate Bond Index to rise to $10.07tn – the highest level since September ’17.

-

Corporate credits saw positive returns across most sectors (Fig 6), but under performed sovereigns as the market turned more risk averse and went up the quality curve. US IG was the best performing sector in the credit space after Asian dollar bonds, returning 2.50% last month. This was mostly supported by falling rates while spreads ended the month mostly unchanged. Strong demand for primary issuances in the IG space also helped lower the borrowing costs for highly rated companies. March saw a 28.57% increase in primary issuances as companies issued $131.28bn worth of debt. IG funds also saw the largest fund inflows in March relative to other sectors. IG funds attracted $13.17bn worth of funds in the month.

Fig 5: Fixed Income sector returns in March ’19 and 19Q1 Source: Bloomberg

-

The key question is whether the Fed’s ‘pivot’, not least in what markets perceived as a ‘dovish’ March FOMC meeting, will prove to be the inflection point in this hiking cycle or, as we believe, a pause. Our view is that the markets have mistaken Powell’s comments to be purely about pausing when, in fact, he explicitly noted that the Fed was data-dependent. We see US macro data as being sufficiently strong to allow the Fed to hike one more time – probably in December 2019, whereas we do see EU data weakness being supportive of the ECB’s recent caution and for lower yields.

-

Whilst we have long failed to find value in higher quality FI (sovereign and IG), even our preferred weightings in US HY FI and Asian HY FI have seen sufficient spread compression YTD to no longer offer much price upside although we would remain invested to ‘clip’ still decent coupons but warn we could see short-term volatility.

-

Tactically, we remain overweight in short-duration paper – be it high quality or HY – as the yield is similar to longer duration paper without the same level of interest rate or default risks.

FX

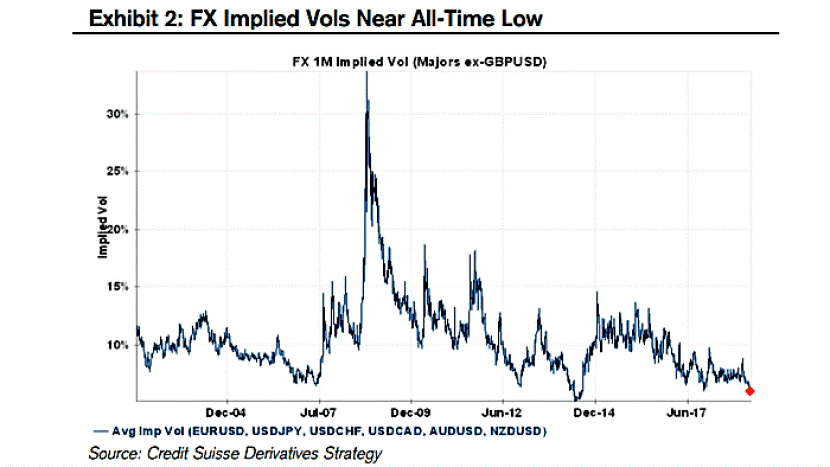

Fig 6: FX implied volatility near all-time low Source: Credit Suisse Derivatives Strategy

-

Volatility in the G7 pairs, bar GBP, has dipped since the start of 2019 as FX markets remain in uncertainty due to key events such as Sino-US trade development and Brexit (Fig 6). EMFX volatility picked up in March, mainly due to BRL, TRY and ZAR experiencing large movements. (Fig 7).

Fig 7: EM FX volatility vs. G7 FX volalitlity Source: Bloomberg

-

The Fed’s dot plot implies that interest rates will remain on hold for the remainder of this year and only improve by +25bps in 2020 and inflation unexpected eased in February. This clarity for the USD has finally come through as markets are no longer pulled by “certainty” (positive market data in Jan/Feb) and “uncertainty” (a “patient” Fed in Jan/Feb). Powell noted that interest rates will remain on hold for “some time”.

-

The Turkish Lira experienced another bout of volatility since Aug 2018. The jump happened overnight and TRY fell 7.50% to 5.84, past a significant key support at 5.50. The Turkish government has reported its suspicion of large foreign banks shorting the Lira. Overnight rates increased to 1300% to prevent shorting. Emergency interest rate measurements taken by the Turkish government failed to suppress TRY weakness.

-

DXY is edging up again towards a key resistance at 97.50 and USD yields bottomed out and it remains, on a relative basis, the best DM economy and that is constructive for the USD. We remain, thus, USD bulls until it is clearer its structural risks (rising fiscal deficit and potential overvaluation) become obstacles.

-

The outlook for GBP, BRL, TRY ZAR and the Argentine peso depends on political developments. An agreed cross-party ‘soft’ Brexit deal would boost GBP towards 1.40 but a no-deal departure on 12th April could sink it back to 1.20. EUR, to a greater extent, will be linked to GBP, but the EU-wide elections could also be a downside risk as it was in ’14.

Commodities

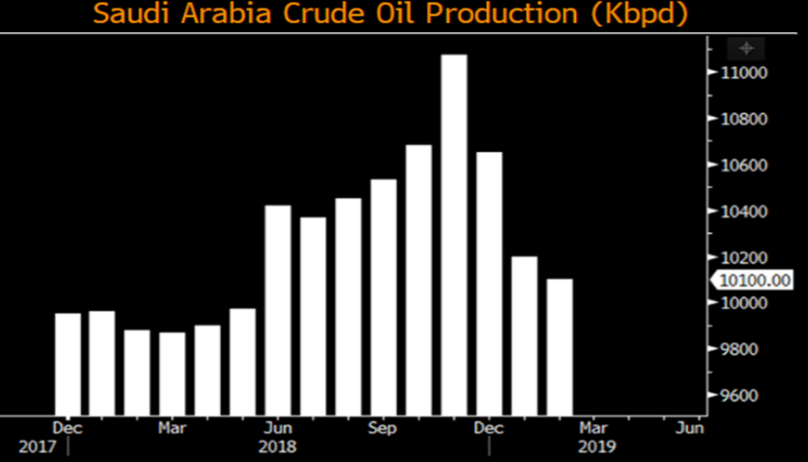

Fig 8: Saudi leads OPEC+ cuts to production Source: Bloomberg

-

Brent crude saw a strong quarter, rising 27.12% YTD and 3.57% in March as OPEC+ cuts to oil production continued. The cartel cut a further 295K/bpd in March, and is believed to continue its commitments to cutting supply and re-balancing the market.

-

Volatile production from countries like Egypt added to supply this month, but we believe that the remainder of OPEC+ countries will eventually catch up and limit their supplies, and this effect should outweigh any of the headwinds.

-

Gold closed mostly flat this month, unable to move past its US$1,352/Oz high in February. This was understandable given the increased risk-on sentiment reflected by the climb in equity markets. This movement in March formed the right shoulder of a Head and Shoulders pattern which started in January.

-

The oil price is being pulled around by OPEC’s (notably Saudi Arabia) supply discipline and regulatory developments on bunker oil relative to rapidly increasing US shale oil production and a slowing global economy impacting demand. In the shorter term, we see the Brent oil price capped around $70/brl but the longer term could see oil prices test $90/brl by 2021 as the effects of the huge 50% fall in capital expenditure since H2CY14 impacts production. Given this, we are trimming our energy exposure.

-

Industrial metals are benefiting from optimism around China’s ability to reflate the economy and from a series of supply disruption that have boosted copper and iron ore at a time the mining giants have proven to be disciplined in capacity expansion, and that could lead to prices moving higher from here in 2019.

CONTACT

We would be more than happy to have an informal chat about these and the other services we offer as well as the current opportunities we are looking at.

Mar 18, 2019 | Articles, Global Markets Update

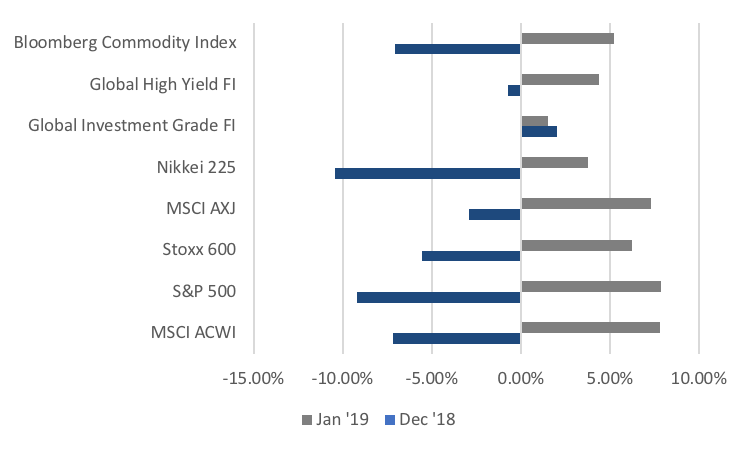

The rally for equities continues after the best January in over 30 years, defying the gloomy consensus seen at the end of 2018 as the S&P 500 (+ 3.0%), NASDAQ (+3.4%) and Dow (+3.7%) gained MoM alongside other major markets which were also up by 2-3%. The exceptions were UK’s FTSE 100 (+1.5%) on a stronger GBP, and a storming move up of 13.8% in China A-shares, including a one-day jump of 5.6% which happened just last week. The week was also the best gain for the index in over four years, as domestic investors’ ‘mojo’ started to reappear (see more below) following last year’s bear market. Stoxx surged 3.9% – in part from very oversold levels – but also helped by a weaker EUR and reduced trade war fears. The S&P 500 beat lowered earnings consensus forecasts for 4Q18 by over 3% to record 13% earnings growth YoY, but elsewhere results were more mixed – Some markets in Asia ex-Japan such as Singapore and Malaysia, instead suffered meaningful earnings contractions. Nikkei’s 3% rise was supported by record share buybacks in corporates’ guidance post-results.

Fig 1: Risk asset performance in Dec ’18 vs Jan ’19 Source: Bloomberg

We are increasingly positive on Chinese shares, whether offshore or A-shares. We like the attractive valuations, proactive policy action, fiscal expansion, PBoC’s easing and improving earnings forecasts in contrast to other large equity markets which are mostly experiencing weaker earnings forecasts, slowing GDP and more limited fiscal expansion. Our base case remains a Sino-US trade deal will occur – most probably in Q2 – and this should underpin CNY below 7.00 if not push it to strengthen further to 6.50 by YE19.

Fig 2: Normalized 10Y chart of SHASHR against the HSI Source: Bloomberg

We are becoming more cautious overall after equity markets and other higher risk assets (such as lower quality HY FI), have rallied strongly from Xmas eve lows. This has taken S&P 500 valuations back into expensive territory, and most other equity regions to fair value from inexpensive – bar PRC equities that remain attractive. Likewise, the rally in credit, with spreads tightening across the board but more so for HY (CCC’s especially) and EM FI, has moved most areas of FI back to fair value whilst sovereign DM FI continue to offer unappealing risk-reward ratios. We see the huge increase in supply of US treasury issuances driving yields higher, with 10Y UST yields testing 3% during 2019. We think that the upside from a likely Sino-US trade deal is mostly priced-in, whereas the risks from an equally likely US imposition of tariffs on global auto imports – at some point in Q2 – is being ignored. We believe that the adage “it is better to travel than arrive”, will apply to the Sino-US trade deal as there is a high chance it will be a partial deal, leaving scope for plenty of future uncertainties as we are only at the cusp of a wider strategic confrontation between the two superpowers.

On a fundamental basis, traditional drivers of risk assets (growth in earnings and GDP) continue to be downgraded (the exception being upgrades to PRC earnings forecasts), and we doubt these will stabilise until 2H19 with 1Q19 set to be quite disappointing. Other positives are also increasingly discounted by markets, namely reduced fears over a Brexit ‘no deal’ outcome, pension reforms in Brazil and a more ‘dovish’ Fed. Admittedly, not all is gloomy as positioning remains light on several indicators, including above average cash levels according to BAML’s PMS survey of the largest global allocators.

We are also seeing offsetting policy action by some governments, notably PRC, increasing fiscal spending, and some central banks turning more ‘dovish’, including the Fed and PBOC, with ECB widely expected to turn more ‘dovish’ too. As a consequence, we have been raising cash and cash equivalents across portfolios and will continue to do so should markets rally further.

Equities

- Trump declared a national emergency over the ‘wall’ in a bid to allay his support base that House Democrats are challenging. Last week we also witnessed the Trump-Kim summit which ended abruptly on an impasse, resulting in both parties going home empty handed without a deal.

- US equities continued up from Jan’s recovery, with all three benchmark indices ending the month firmly positive as IT (+6.63%) and Industrials (+6.06%) led gains in the S&P 500 (+2.97%), while the Dow and Nasdaq were up 3.67% and 3.44% respectively. Markets were also somewhat sated after Powell reiterated the FOMC’s patient approach and sensitivity to capital markets, but also that the Fed would hold a much larger balance sheet than it did pre-crisis.

Fig 3: MoM moves across S&P 500 sectors Source: Bloomberg

- S&P 500 has reported earnings for 4Q18 – 72% of companies have beat estimates to an aggregate earnings surprise of 3.59%, while the aggregate growth rate of earnings came in at +13.07%, in-line with the estimate of +12.10% at the end of FY18. Unsurprisingly, elevated oil prices helped the Energy sector to the highest earnings growth of all, at +93.5%.

- For 1Q19, the aggregate analyst prediction is a -3.2% decline in earnings. MS has warned that FY19 could see a possible earnings contraction after a string of forecast downgrades, trimming their own estimates for FY19 EPS growth to just 1% from an earlier 4.3%. The house maintains their S&P 500 price target of 2,750 at YE19. Consensus FY19 EPS (Earnings Per Share) growth is estimated at +5%, but there remains a risk of an overall contraction although analysts see a recovery from weaker H1 earnings by Q4 coming from an easier base of comparison.

- European equities saw broad-based gains, with the Stoxx 600 climbing 3.94% in the month. Materials (+7.26%), Chemicals (+6.07%) and Insurance (+6.19%) led gains across sectors, while defensives like Utilities (+0.27%) and Telecommunications (-0.01%) were visibly weaker. Real Estate (-1.76%) was the only sector to see a decline.

- Stoxx is being torn by upside from relatively cheap valuations against the S&P 500, and its far worse economic performance that could result in an earnings contraction. EU SMEs are more vulnerable to a weaker economy, but could rally in the short-term if ECB becomes more supportive. EU will be especially impacted if US imposes auto tariffs that would hit the large EU auto OEMs hard. Our base case is Trump will impose tariffs, if more to appease his support base, but would lift them quickly to avoid damaging the US economy – a bit akin to NAFTA.

- Shares in Asia trended higher on optimism around trade, as rhetoric (mostly from the US) and sentiment on a near-term trade deal grew increasingly positive particularly toward month-end. The MSCI Asia ex-Japan’s +2.05% MoM gain was completely overshadowed by the run up in China A-shares (+13.91% MoM), which have surged over 20% from early Jan lows into a technical bull market.

Fig 4: SHASHR outperformance against other indices in Asia Source: Bloomberg

- The Nikkei also managed to climb 2.94% last month, but on the back of a weaker JPY which saw the index only up +0.62% MoM in USD-adjusted terms. GDP growth in 4Q18 came in at 1.4%, with IMF forecasts pointing to a further slowing of economic momentum in ’19. Corporate profitability has, however, stayed near record levels, and risks around deflation have decreased significantly.

- Over the course of this month, the delay of trade tariffs were confirmed, alongside subsequent reports which pointed toward substantial progress in the ongoing negotiations with March 27th now being suggested as the tentative date for Trump and Xi to sign off on a deal. However, the US’ point negotiator Lighthizer did temper market expectations later in the month, commenting that ‘much still needs to be done’ before an agreement could be reached.

- We see a lot of good news discounted by gains in Asia ex-Japan and EM equities YTD, with valuations of MSCI Asia ex-Japan back at historical levels and earnings forecasts still coming down. Given this, there is a stronger case to turn more defensive and move tactically into cash. An exception – see above – might be A-shares, as opposed to a number of H/HK shares looking more vulnerable now.

Fixed-Income

- US Treasury yields traded within a tight range for most of February before better-than-expected 4Q18 GDP numbers led UST 2Y yields to end 5.65bps higher at 2.51%, and UST 10Y yields to end 8.67bps higher at 2.72%. The yield curve saw a parallel shift downwards across the 2Y to 10Y period, with the 2Y10Y spread increasing by only 3bps over the month. Technically, UST 10Y yields found support at 2.63%, having failed to break below the level despite testing it four times.

- European sovereign bonds were mixed. Bund yields saw weakness throughout the month following multiple weak economic data releases, hitting a low of 0.08% before ending the month at 0.18%. Strong demand for new Italian and French debt issuances followed a series of strong European sovereign bond sales this year.

- PIMCO and CS both expect UST yields to rise in order to absorb the massive extra issuance needed to fund the fiscal deficit, with both expecting UST 10Y yields to reach 3% in 2H19. Foreign buying is impacted by a high cost of hedging USD, effectively eliminating most of the nominal yield pick-up available.

- The Fed may have erred by switching from being too ‘hawkish’ in Oct last year to being too ‘dovish’ following the Q4 swoon in capital markets. With the US economy seemingly still in rude good health and markets having recovered, there lies a growing possibility that the Fed might surprise complacent FI markets by reasserting its 2 rate hikes in the ‘dot plot’ guidance, even if technical factors instead support an end to balance sheet reduction.

- There is polarisation around whether to move up the credit curve to avoid a coming credit crisis. To some extent, this is linked to recession risks over the next 12-18 months. Those who doubt this would prefer the risk-reward in HY and EM FI. What is worth noting, is that PIMCO thinks the rating agencies are far too optimistic with their ratings, plus we know the majority of issuances are covenant-lite, and that reduces recovery rates.

FX

- FX volatility has fallen significantly, with the DXY barely moving and most other currencies stuck in their respective trading ranges. GBP, AUD and JPY were the exceptions.

- USD – January’s dip was compensated by gains in a risk-on environment as political tensions eased up. Overall, there are mixed sentiments for the dollar as investors juggled between Powell’s dovishness and positive US economic data.

- JPY weakened sharply against the USD last month to test, and weaken through, key support at 111.50, as the BOJ reiterated its accommodative monetary policy stance, macro data disappointed and concerns grew about global auto tariffs which Japan would be significantly impacted by.

- The EUR touched a monthly low of 1.123 on fears of auto tariffs. ECB and others, as IMF, have revised growth projections lower to 1.7% for 2019. The EUR has shifted its trading range from 1.13-1.18 in to 1.125-1.15, weighed down by potential snap elections in Italy as well as Spain. Brexit also weighed on the EUR.

Fig 5: GBP moves on Brexit Source: Bloomberg

- So far this year, Brexit has seen the GBP trade in a wide range of 1.27 to 1.33. It started the month at 1.310, traded to a low of 1.277, but ended the month at 1.326, on increased hopes a ‘no-deal’ option will be rejected by Parliament. It recovered above its 200DMA at 1.30 after falling below this level earlier in the month. Markets are currently pricing in a potential second referendum, which will add strength to GBP. 1.33 remains a key resistance level.

COMMODITIES

- Brent crude gained 6.69% through the month, breaking through its key resistance at US$64/bbl on continued commitment to production cuts from OPEC+. Prices were also supported by reports that the group could move toward a more formal agreement, which could see the cartel control 66% of the global supply of oil and over 90% of spare capacity.

Fig 6: Gold (green line) tapers off, while Iron Ore (yellow) hits all-time high Source: Bloomberg

- Gold broke out earlier this month to test a high of US$1,346.71 /Oz, but failed to test the key resistance level just above $1,360/Oz. It then fell sharply thereafter on a combination of profit-taking and rising UST yields, alongside a stronger dollar which weighed on the precious metal. It broke through support levels at $1,320 in late-Feb, and $1,300 in early March to where it is currently testing the next key support at $1,280.

- Iron ore hit its all-time-high after the Vale mine disaster abruptly tightened global supply, whilst PRC’s implicit ban on Australian coal imports created movements in thermal and coking coal and again, highlighted the dangers of being a major supplier to PRC as the ban was linked to Australia’s decision to exclude Huawei as a supplier to 5G telephone systems on national security grounds.

- We remain constructive on oil as we believe there are supply-side restrictions that will underpin prices above $60/brl for Brent. The super OPEC+ cartel will have much greater pricing control than OPEC did, and thus will more easily be able to counter rising supply from US shale oil production to retain their status as a price leader. US shale oil producers will remain a force – just this week, both Exxon and Chevon said that they would triple oil production by ’23 at their respective Permian basin fields. It is material as Exxon expects to produce over 1m bpd by then, with Chevron not too far behind.

- Another support for oil prices is the continued capex discipline of the large, integrated oil companies, as spending remains 40% below the peak in 2014, with estimates that it will rise just 5% this year. If this continues, there is a genuine risk of a supply crunch by as early as next year that could see oil prices jump to over US$90/bbl.

CONTACT

We would be more than happy to have an informal chat about these and the other services we offer as well as the current opportunities we are looking at.

Feb 18, 2019 | Articles, Global Markets Update

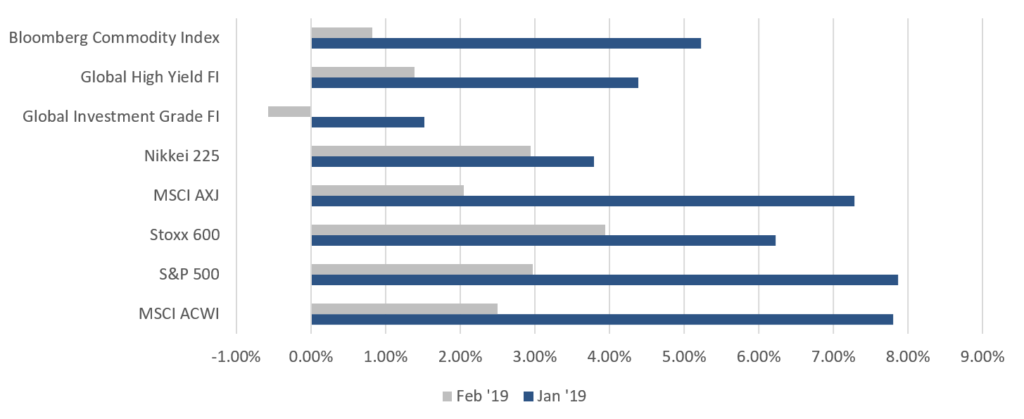

Risk assets rebounded strongly in January after a horrific December (Fig 1). The MSCI ACWI gained 7.80% in January, its largest gain since October 2011. This came after December’s fall of -7.17%, the second-largest fall since May 2012. A more significant comparison can be seen in the US, with the S&P 500 seeing its best January since 1987 after its worst December since 1931. Similarly, global investment grade (IG) fixed-income (FI) gained 1.52% in January while global high yield (HY) FI gained 4.39% following December’s 2.52% and -0.75% respectively. The VIX index has also been registering higher ‘lows’ in January, adding to signs that volatility is indeed returning.

Fig 1: Risk asset performance in Dec ‘18 vs Jan ‘19 Source: Bloomberg

Risk assets were supported on two fronts in January, with the first being optimism around the US-China trade situation. The first major round of trade talks since the Trump-Xi truce took place at the start of the month and ended on an optimistic note. Our base case remains that a narrow trade deal will likely be done, though the US is after a wider deal that addresses structural issues. A dovish Fed also provided support to risk assets, alongside a weaker dollar for the most part of January. Within FX, Asia ex-Japan (AXJ) pairs were the main beneficiaries of the USD weakness as they rebounded from their 2018 lows. There was also volatility around the GBP as it followed Brexit headlines.

Tactically, we remain cautious as fundamentals continue to deteriorate, bar a robust US economy (January’s ISMs and NFP numbers imply Q1 GDP growth of c. 3%), as we continue to see global GDP numbers being downgraded to c. 4-5% growth, from +10% at end of Q3FY18. Historically, equities struggle in the face of deterioration in EPS and GDP forecasts so the billion-dollar question is – what are markets discounting? If the December fall was overdone and predicated on a recession and EPS contraction, then one wonders at what point will this rally run out of steam (barring a US-China trade deal later this month), given that investors have repositioned quite aggressively since Christmas Eve, which has reduced this underpin.

Other than trade, the only other clear positive is that almost no one is positive, with a majority remaining uncertain and fearful. It continues the tradition of this being one of the most hated bull markets and economic expansions of all time, just as these are one of the two longest such periods. Equity bull markets and economic expansions do not die of old age and it is hard to see signs of the euphoria typical of the final stages of a bull market.

Another factor we strongly think is being ignored by markets, is the continued evidence of a strong pick-up in fiscal spending that appears to be globally synchronised. No doubt this is helped by the fact that we are in election years in parts of AXJ, coming into European Union (EU) elections in May, and are at the start of the US election year campaigning. We expect the Federal fiscal boost to continue well into 3Q19, with a large chunk of tax rebates for households being mailed out in the next few months to help consumption.

We would note (rather cynically) that based on history, the prospect of additional, and thus higher, Federal spending into elections is quite high, notwithstanding a consensus view that partisan politics will stymie extra spending in an Infrastructure Bill. Markets rarely seem to understand that fiscal spending tends to be dynamic and we have evidence that fiscal spending is picking up globally, be it from the EU (Germany, Italy and France are all set to spend substantially more as a percentage of GDP as most likely will UK), China, India (we are seeing Modi’s Bharatiya Janata Party government boosting handouts to farmers) or Japan (the government is expected to boost spending, including a package to offset the GST-hike set for October this year). Should a US-China trade deal materialise, these drivers, as they materialise in better GDP numbers by 2H19, could power the next leg of the rally in risk assets in the medium-term but stoke inflation in the long-term.

Equities

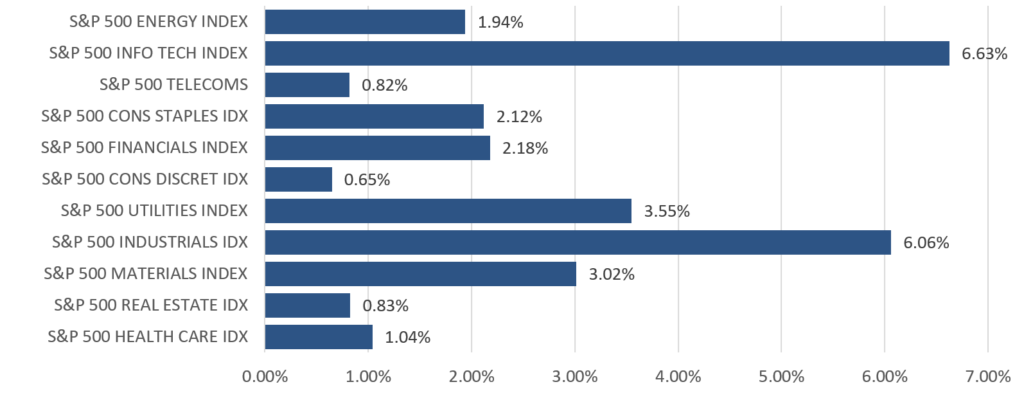

- The S&P 500 (+7.87%) saw a broad-based rebound from December’s decline, although gains varied as Energy and Industrials powered ahead, leaving defensives like Utilities trailing behind (Fig 2). The Technology sector was slightly mixed after heavyweights such as Facebook guided for lower growth, weighing on sentiment across the sector. However, others such as IBM rallied after posting strong earnings beats and better-than-expected guidance for FY19. The Dow Jones (+7.17%) and Nasdaq (+9.74%) also experienced a similar rally in January.

Fig 2: Defensive sectors lagged in the S&P 500 Source: Bloomberg

Fig 2: Defensive sectors lagged in the S&P 500 Source: Bloomberg

- The STOXX 600 (+6.23%) also joined the rebound in global equities, with Telecommunications being the only sector to see a decline. This came after concerns over alleged spying by Huawei led to companies pulling out of ongoing 5G infrastructure developments (on top of pressure from the US), but also as investors grew weary of further delays and potentially higher costs in alternative providers. Within the index, just over 30% of companies have reported earnings, with 54.63% reporting an aggregate beat of +8.85%, and an aggregate earnings growth of +4.19%. On the other hand, over 44% of these companies saw earnings surprise to the downside.

- Nikkei (+3.79%, or +5.31% in USD adjusted terms) had a relatively poor performance against the broader MSCI AXJ (+7.79%). While the Shanghai Composite Index (+3.65%, or +6.40% in USD adjusted terms) lagged behind on continued USDCNY strength, the recovery in sentiment on Chinese equities was evident in the Hang Seng Index (+9.33%) which led gains across Asia.

- It is important to highlight that USD rates, relative to AXJ, are a good indicator in determining returns for equities in this region. Credit Suisse released an analysis some months back that showed AXJ equities outperforming their US counterparts by over 5% when the USD weakened by 5% or more, and vice versa when the USD strengthened. JP Morgan (JPM) backs this up in a research paper, showing that AXJ outperformed 100% of the time and on average by around 20%. Interestingly, many FX strategists are now predicting the USD to weaken significantly against currencies in AXJ, with the USD having been on a downward trajectory since October.

- A weaker USD coupled with far more stability in US equity markets (that have moved away from trade and bear market concerns) provide a scenario which is supportive for equities in AXJ. On top, EPS downgrades in this region over the past three months came in at -3%, which was less than the -5% decline in estimates for the S&P 500. The tail risk remains, however, that this could change rapidly, and that this market requires a close eye and strict risk controls.

- Looking specifically at China, it appears that markets seem to underestimate the degree of liquidity easing, tax cuts and reflation, in the same way that markets had arguably overestimated Trump’s one-off tax reforms in the 18H1. In our view, these are likely to cushion, if not support Chinese equities, and are drivers that other markets seem to be lacking.

- It was a somewhat eventful month for the US, after we saw resolution to the longest-running US government shutdown, but also as some economists continued to trim US GDP growth estimates for 18Q4 and 19Q1. Powell himself raised concerns over the potential impact of the shutdown, and some estimate that the shutdown may have trimmed 40bps off 19Q1 GDP growth alone.

- It is likely that markets continue to underestimate US political risks, with the recent government shutdown potentially a foreshadowing of an even larger tussle when government funding runs out in September. Additionally, developments around the Mueller investigation also point to a genuine risk that he may indeed have a ‘smoking gun’ tying Trump to the Russians, which could prompt the latter to shut down the investigation entirely. Either scenario could potentially trigger a constitutional crisis. The greater concern for markets, is Trump’s unpredictability which ratchets up as he comes under pressure, particularly if it relates to legal or constitutional pressures.

- Evidently, these looming risks are sufficiently negative to have significant implications for the US market, more so if we see both intensify at the same time which is not at all unlikely given Trump’s history. We need to remain cautious around 19H1 beyond these two risks as they exacerbate the broader US/global GDP slowdown, weaker EPS growth, and uncertainty over whether Powell made a mistake in tightening too far. Our base case remains that these fears are exaggerated and will likely be reduced over time as hard data provides greater clarity over direction and quantum.

- Given this, we are cautiously optimistic on a positive outcome on trade in the near term. Trump continues to face pressure from blame over the recent shutdown, weakness in the US equity markets have investors questioning the US growth outlook, while Xi is likewise tackling the impact of multiple factors which have led to China’s slowing economy. Both have incentive to ensure that some degree of progress around trade negotiations are secured at least in the near-term.

Fixed-Income

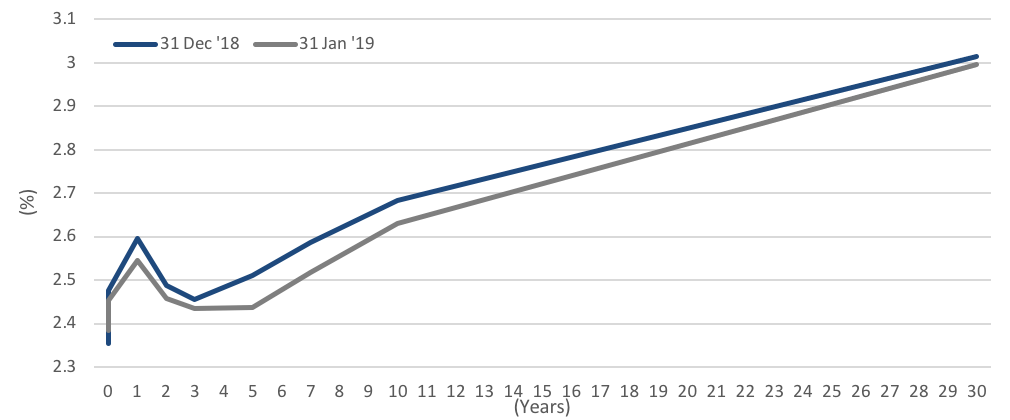

- Sovereign debt was relatively flat in January as the market turned mostly risk-on. US Treasury (UST) yields rose sharply at the start of the month as investors turned risk-on following a blowout in December’s NFP numbers and rotated out of the safer government debt. The UST yield curve saw a parallel shift downwards, with greater falls in yields in the 5Y to 10Y period (Fig 3), following a dovish announcement by the Fed that led markets to think that rate hikes might be on hold. Bunds sold off early in January, along with USTs, but yields trended lower through the month as weaker economic data weighed on sentiments.

Fig 3: Yield curve shifts lower in January Source: Bloomberg

Fig 3: Yield curve shifts lower in January Source: Bloomberg

- Credit also saw a positive return across all sectors, as spreads eased lower after reaching 2016 highs in December. The risk-on mood saw US HY gain the most, finding support from fund inflows, steady US economic data, rising oil prices and a dovish Fed. The Bloomberg Barclays US HY index gained 4.52%, its largest January return since 2009 (Fig 4), with CCC-rated bonds jumping 5.29% while BB yields fell to a 4M low of 5.32%.

Fig 4: Junk bond comeback Source: Bloomberg

Fig 4: Junk bond comeback Source: Bloomberg

- Bloomberg data also showed EM debt issuance reaching $172bn MTD. This is more than any January on record as borrowers took advantage of the strong demand from the turn in sentiment toward risky assets in January.

- We think Powell’s dovish comments might not be entirely a good thing. Powell seems to have overcompensated for 4Q18, and is simply giving the markets what they want to hear with no clarity. The Fed’s pandering to markets led several sell-side banks like GS, JPM and BofAML to think that the UST 10Y yield might have peaked for this cycle, causing them to cut their year-end projections.

- However, we think the US economy remains robust, as evidenced by the strong January NFP and ISM manufacturing PMI numbers. This, coupled with the US Treasury’s expected issuance of $365bn in debt in 1Q19 ($8bn more than its previous estimate) to finance its widening deficit, should provide upside pressure for UST yields.

- We maintain our conviction in shorter-duration debt given its defensiveness against interest rate risk. We continue to like HY debt as we believe there is still room for growth, and fundamentals for the sector remain strong. Analysts have also expressed a similar view, with the likes of Wells Fargo and Barclays upgrading their annual forecasts of US HY returns to 9.9% (from 6%) and 6.5%-7.5% (from 3.5%-4.5%) respectively.

FX

- A dovish Powell caused weakness in USD during the start of January, which has been reflected in the recovery of AXJ currencies after last year’s decline. The DXY tested 95.300 twice – once during the first week of January and the other on 30th This level is just above the 200DMA found at 95.371. We remain moderate dollar bulls on the basis that the US economy remains strong and positive data will lead the Fed to resume raising rates.

- JPY strengthened to 108 in the first half of January on dollar weakness, which is also a resistance level, ignoring the flash crash to 104.96 early January which resulted from trading on thin liquidity. Unsurprisingly, BOJ left rates unchanged and lowered its near-term GDP forecasts. This, along with relatively stronger data out of the US are factors that could lead the JPY lower to 110.

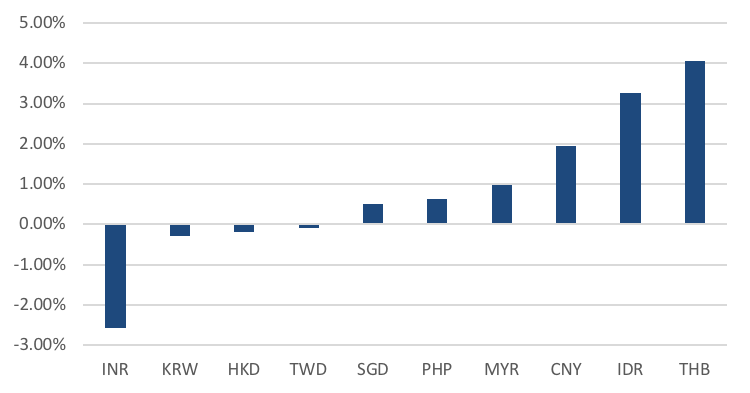

- Amongst AXJ FX, THB (+4.06%), IDR (+3.27%) and CNY (+1.94%) have been leaders YTD (Fig 5). Strength from the Thai baht has been attributed to the 25bp rate hike in December as well as an increase in Thai equity purchases from global funds.

Fig 5: AXJ FX total returns against USD as of 6th Feb ‘19 Source: Bloomberg

Fig 5: AXJ FX total returns against USD as of 6th Feb ‘19 Source: Bloomberg

- CNY strengthened greatly to c.6.70 in January on dollar weakness and optimism around trade, weakening toward the end of the month as this sentiment waned. A few data releases also added to uncertainty over China’s economic trajectory, which also weighed on the currency.

- The course for AXJ FX will be dependent on three aspects, the Fed (US data), the CNY (US-China trade negotiations) as well as the Brent price. We may see some downside pressure over the next month or two until we see a recovery in macroeconomic data. USDCNY’s bounce off its 6.70 resistance in January (and a move back above the 200DMA) implies this. THB will likely hold against its 31.132 resistance, following BOT’s recent decision to leave rates unchanged.

- Much of the directionality for the EUR or the GBP lies in the fate of Brexit. We think that the BoE will unlikely change its monetary policy until there is clarity around Brexit. We expect an extension to Brexit’s deadline, hence reducing the likelihood of a ‘hard’ Brexit. This should be supportive for the GBP in the medium-term.

COMMODITIES – REVIEW

- Brent oil recovered from its 52W low of 50.47 in December to end January at 61.89 on the back of a weaker USD. Venezuelan sanctions contributed to the bullish sentiment around oil, with the cold spell in the US boosting fuel demand. This 15.04% MoM gain was its largest since April 2016, but it now struggles to move past a technical resistance level of 62.80.

- The oil rally since December’s low has also led to significant short covering. ICE data showed that shorts fell 27% in the week ended 29thJanuary to their lowest point since October ’18, while long positions held by hedge funds increased by 15%.

- Oil will remain attractive below its technical resistance of 62.80, but the direction of oil will require clarity on key issues such as China’s economic slowdown and in turn, AXJ’s demand for oil; US’ output and OPEC’s ability (and Russia’s willingness to cooperate) to pull through with their cutbacks in production. These short-term headwinds may only be rectified as we move past 1H19.

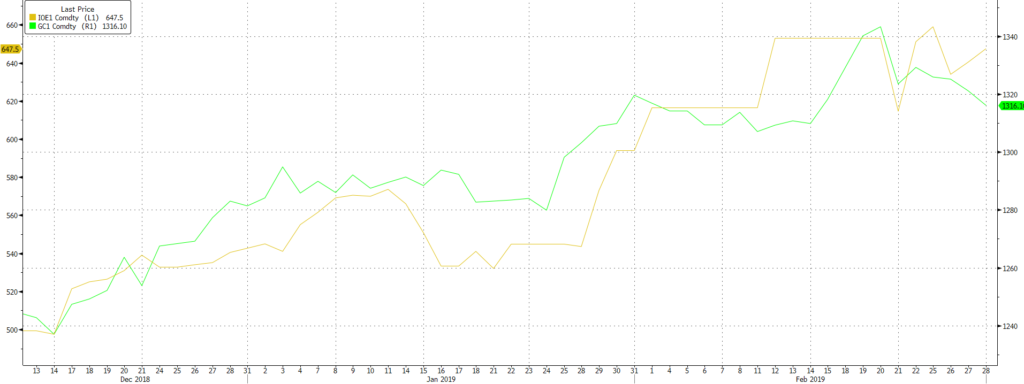

- Gold began a new trend, borrowing strength from uncertainty and increased volatility in the markets as we ended 2018. The dim outlook for the dollar at the start of ‘19 also supported gold through the month, as it broke above the $1,300/oz level to end the month at $1,321. However, it failed to break significantly above the $1,320/oz level and pared some of the gains in the first few days of February (Fig 6).

Fig 6: 1Y gold chart Source: Bloomberg

Fig 6: 1Y gold chart Source: Bloomberg

- Dollar strength was the main contributor in Gold’s recent losing streak, but the precious metal has followed its 20DMA rather closely, which suggests that the uptrend may still be intact (Fig 6).

- With investors betting that the Fed may now be on hold, and as the global economy slows and volatility picks up, gold offers an alternative safe haven to FI. Last year, speculative positioning was reduced substantially and central banks bought the most gold since ‘71. With these in mind, we may see gold push higher to test multi-year highs of around $1,360/oz.

CONTACT

We would be more than happy to have an informal chat about these and the other services we offer as well as the current opportunities we are looking at.

Jan 10, 2019 | Articles, Global Markets Update

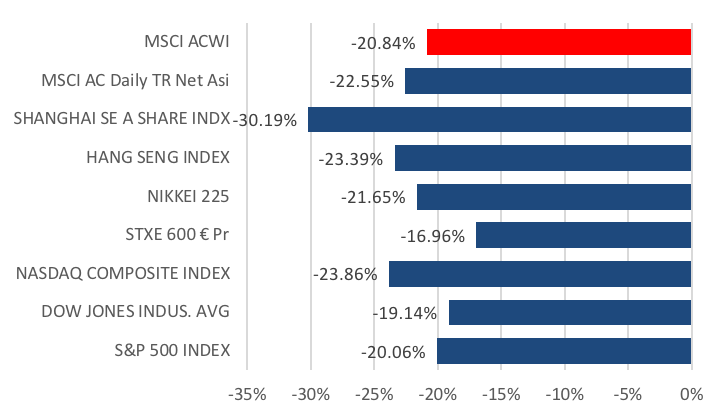

Equities fell momentarily into a technical bear market on Christmas Eve amidst growing concerns that the Fed is raising rates into a slowing global economy, evidenced by weaker manufacturing and other various economic data released over the month. Thin trading through the month worsened the losses. The MSCI ACWI fell to 435.90, 20.84% off its 52W high, before ending the year at 455.66 to register a 11.18% loss for 2018. Most major equity indices also fell into a technical bear market over Christmas (Fig 1). However, the Fed also trimmed its 2019 rate increase projections to two increases from three and lowered the long-term equilibrium Fed rate to 2.75% from 3%.

Fig 1: Global equities fall into bear market over Christmas Source: Bloomberg

There were several developments in the Sino-US trade situation as well. In the first month after Trump and Xi’s meeting at the G20 conference, we saw China cutting US auto tariffs from to 15% from 40% and making a huge purchase of US soybeans while Trump cited huge progress in trade developments after a phone call with Xi. There were concerns that the arrest of Huawei’s CFO might jeopardize the discussions, but these worries were short-lived.

Brexit developments, however, took a turn for the worse earlier in the month after May delayed a parliamentary vote on the Brexit deal, survived a vote of no confidence and stepped up preparations for a ‘hard’ Brexit. This chain of events led to a volatile month for the GBP, which traded -2.13% to a low of 1.2478 before ending the month almost flat.

We suggested last year might start well, turn tricky and become difficult, but we were surprised by the speed of the changes and, in particular, the severity of the fall in the S&P 500 in December. 1969 was the last time all asset classes struggled and cash outperformed. Our base case for 2019 is it will likely be an uncertain and volatile start but, as we potentially get more clarity over key risks, conditions may become more constructively for risk assets in 19H2.

We are not bearish and do not see a ‘smoking gun’ that will devastate markets. We believe markets are suffering another growth scare often seen since 2010, with 2017 the exception. We doubt a recession is imminent in the USA or globally, nor do we anticipate an earnings contraction either. We believe markets have already discounted a lot of bad news but are ignoring some positives, such as the largest, synchronized fiscal expansion since 2010.

Our base case is predicated on these assumptions: A Sino-US trade deal is desired by both the USA and China; a ‘soft’ Brexit is the probable outcome, albeit it could be delayed; Italy will agree a budget deal with the European Commission (EC) and remain in the EU; China will support its economy sufficiently to defend a 6%+ GDP growth and ensure CNY’s stability; the Fed will raise rates two times in 2019 and then be driven by the data; and that the US GDP will grow at a solid 2.5% in 2019 and global GDP growth will be solid. Should we be wrong and a ‘bear’ market in equities occur, we see a probable Powell ‘put’ limiting the downside.

Tactically, we see the first few months of 2019 as a ‘tricky’ period. Global GDP growth and EPS will slow, and it may take until late April – with Q1 results coming out – to provide jittery investors with a better clue as to the direction for US/global EPS. Likewise, we need to see the spate of GDP downgrades stabilize. Whilst we remain optimistic a trade deal will occur, Trump’s negotiating style may result in fears of a global trade war, including the risk of global auto tariffs, remaining high and this is most investors’ key risk.

Equities

- December was particularly harsh, as all three major indices in the US were down close to -9% over the course of this month. The S&P 500 saw a broad-based decline across all sectors (Fig 2), with Energy (-12.82%) leading losses as global oil prices declined on high inventory levels and weaker economic growth outlooks. Financials (-11.45%) and Industrials (-10.81%) were also particularly hard hit, no doubt a result of dampening expectations for interest rates, and the ongoing trade-related issues with China.

Fig 2: All S&P 500 sectors ended December lower Source: Bloomberg

Fig 2: All S&P 500 sectors ended December lower Source: Bloomberg

- The Stoxx 600 had a relatively better month than Wall Street, falling -5.55% MoM to finish the year -13.24% lower. The index saw a broad-based decline, with Retail (-7.98%), Banks (-7.70%) and Autos (-7.21%) leading losses. It was also a down month for the FTSE 100, which fell -3.61% MoM.

- China A-shares fell 3.65% in Dec to end the year 24.60% lower, while the HSI likewise declined 3.78% to finish FY18 14.60% lower. Despite some positive developments around the 90-day US-China truce, an early rally by Asian equities quickly subsided as negative sentiment continued to weigh on investors, as evidenced by the -2.93% MoM decline in the MSCI Asia ex-Japan Index. Data releases did not provide much needed respite either – in China, industrial profits fell for the first time since 2015, as November trade data surprised on the downside as exports struggled despite tax rebates and a weak currency, while a slowdown in imports highlighted slowing global trade and a weakness in domestic growth.

- China’s Central Economic Working Conference was also held this month, with the outcome being a renewed focus in stabilizing economic growth through policy stimulus. There was also quite a bit of focus on PBOC’s newly announced Targeted Medium-Term Lending Facility, aimed to provide low-cost liquidity to smaller companies.

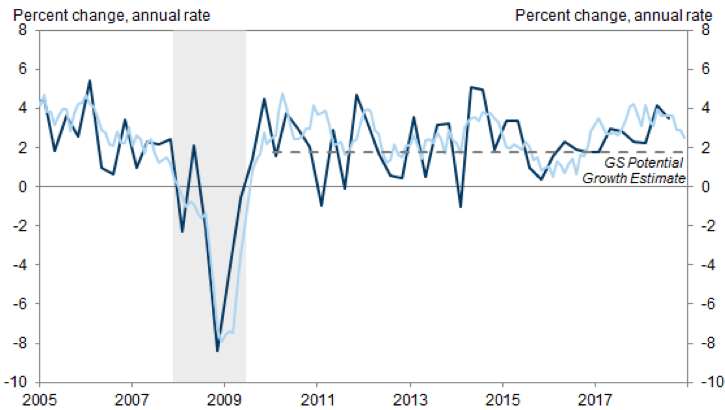

- The fundamental question for 2019 is whether the deteriorating growth environment will negatively impact US growth. The short answer is yes, but not materially. In a recent report, Goldman Sachs (GS) notes that slower global growth could affect US growth through 1) the reduction of demand for US exports 2) a reduction of US business investment spending and 3) tightening of US financial conditions. While we might see this play out over the course of 1Q19 (and GS predicts that this could trim 0.4% off US growth), the economy should be strong enough to cope with this negative drag (Fig 3)

Fig 3: US Growth Remains Solid Source: GS Global Investment Research

- Tail risks continue to be an escalation in the Sino-US trade dispute, and a sudden spike in inflation which could force the Fed to raise rates far more aggressively than the market currently expects. UBS predicts that this could result in a flat or inverted yield curve somewhere in the middle of the year, followed by sell-offs in the equity market, which could set the stage for an early recession in 2020.

- Brexit remains the biggest geopolitical risk in the Eurozone, because the outcome remains largely uncertain. While the impact may be more contained within UK/EU, odds are for a weaker and potentially volatile GBP as the process drags on, dampening Capex prospects and continuing the overhang on GDP growth. The next key date to watch is the week of 14thJanuary, where May’s delayed ‘meaningful vote’ is scheduled to take place.

- Earlier in September, we posited that China’s policymakers faced an increasingly difficult balance between policy decisions, and that every subsequent move would result in elevated costs and risks. Daiwa highlights that we saw this unfold numerous times over the past few months, as the PBOC took to defending the CNY at the 7.00 mark. While a fall below this level would have negative implications (i.e. capital flight), the result has been 1) denying a downward adjustment which would have been supportive of export competitiveness and 2) Offsetting a good deal of stimulus effects from both fiscal and monetary measures, as we have observed from the continued weakness in data toward the year-end.

- We expect more guidance by the PBOC in early March, particularly around growth targets which are slated for announcement during the National People’s Congress meeting. It is widely expected that the government will maintain an expansionary fiscal policy and much like 2018, the consensus is for another four 50bps cuts to the Reserve Requirement Ratio this year. The positioning of the Chinese government has clearly turned toward an easing stance with more measures expected to come in 2019.

Fixed-Income

- Sovereign debt rallied sharply in December as weak economic data raised concerns of a global growth slowdown and increased demand for safe haven assets. The UST yield curve shifted lower through the month, with the 2Y UST yield falling 29.87bps, the most since June 2016, while the 10Y UST yield fell 30.37bps, its largest decline since January 2010. The 2Y-10Y spread remained largely unchanged at 19.64bps at the end of December. The Bunds yield also fell 7.1bps over the month and continued falling in the first week of January to reach its lowest level since April 2017. However, sovereign yields saw a pick up on 5thJanuary after a strong NFP number and Powell’s reassurance that the Fed will not rush to raise interest rates helped ease concerns.

Fig 4: Bond spreads reach highest levels since ’16 Source: Bloomberg

- Credit also saw positive returns across the sectors, with spreads reaching its highest levels since 2016 (Fig 4). US IG bonds gained the most in December, with the Bloomberg Barclays Global US Corporate Total Return index up 1.47%, despite IG bond funds seeing six straight weeks of outflows (Fig 5). Investors withdrew $17.8bn from IG bond funds in December. This helped pare its losses in 2018 to -2.51%.

Fig 5: US IG bonds see six straight weeks of outflows Source: Bloomberg, Lipper

- HY debt underperformed in December as it tracked equities and oil prices lower. US HY performed the worst in December, with the Bloomberg Barclays US Corporate HY Total Return index falling 2.14% while spreads widened to 526bps, just shy of the 30M peak set on 27th December’s performance caused the US HY sector to end the year -2.08%, resulting in its worst year since 2015. HY bond funds also saw seven straight weeks of outflow, with $8.2bn withdrawn in December.

- However, issuance dried up in December. US IG bonds went through the last three weeks of December without any issuance and ended 2018 with $1.08tn in issuance, falling 11% from ‘17’s $1.21tn amidst a combination of higher borrowing costs and overseas cash repatriation. There was also no issuance of US HY debt in December, the first time in over 10 years.

- US HY now appears to be of value, given the levels it is currently trading at – 7.95% yield with a 5.26% spread. Sell-side forecasters are expecting US HY to bounce back in 2019 (Fig 6). Key drivers of US HY bonds – default rates, earnings, GDP growth, corporate cash flow – also look to be generally supportive. However, despite its cheaper valuations, US HY presents higher risk given the near-term uncertainty, higher volatility and tighter financial conditions. BofAML raised its US HY default rate estimate for 2019 to 5.5% from 4.25% and suggests a risk neutral spread of 5%, relative to 5.3% currently. It is necessary, even more so now, to be selective of better-quality names in this space. Given the amount of uncertainty in markets now, we continue to recommend sticking with short duration debt.

|

US HY ’19 Expected

Returns (%)

|

Leveraged loans ’19

Expected Returns (%)

|

| JP Morgan |

3.25 |

6 |

| BofAML |

2.4 |

4 – 5 |

| Citibank |

2.7 |

3.3 |

| Morgan Stanley |

0.5 |

1.3 |

| Wells Fargo |

6 – 7 |

3 – 4 |

| UBS |

5.6 |

4.3 |

| Barclays |

3.5 – 4.5 |

4.5 – 5.5 |

Fig 6: Sell-side expectations for US HY and Leveraged Loans Source: Bloomberg

- European credit will likely be a difficult space to trade in this year as investor sentiment wanes. This year, the region faces risks in the form of Brexit uncertainty and a slowdown in global and European growth. In addition, with the ECB stopping net asset purchases and only reinvesting its maturing holdings, it removes a safety net of sorts, worsening liquidity in the space.

FX – REVIEW

- December’s biggest move in currencies was the USDJPY, which fell 3.42% in December, and continued its decline in early January to a low of 104.87 before recovering back to the 108 region. The decline came as disappointing US data sparked fears over a US slowdown, spurring a risk-off move to the ‘safe haven’ JPY.

- The JPM EM FX Index was mostly unchanged at 62.221, falling 0.5% for the month. Within the index, there was notable resilience in the USDTHB, which instead moved -1.02% from 32.885THB to 32.548THB, strengthening even further against the Dollar in early Jan to 31.965THB.

- This month also saw the DXY break its 50DMA support at 96.6 to fall -1.13% in December, finding a new support from its 100DMA at the 96.0 level. The EUR gained 1.33% against the dollar for the month, but also mostly from general Dollar weakness over slowing growth in the US.

- The base case this year is a complicated one, but we are more inclined to think the Dollar will likely end the year in a weaker position. While appearing to be overvalued on a fundamental basis, there are still too many reasons why uncertainties will keep its ‘safe haven’ status supported especially over the first half of the year.

- Moves in the GBP will still largely be dependent on news surrounding Brexit. As discussed earlier, a no-deal scenario could potentially send the sterling significantly lower from where it is now, and that situation might present a short-term opportunity for a tactical trade. Our base case is more likely a soft deal (rather than a no-deal situation), which should support the sterling as well as the euro.

- We are cautiously optimistic that EM Asia currencies could rise against the dollar over the next few months, if not more so in the second half of 2019. As we have witnessed over the course of 2018, this will also largely depend on how the CNY moves, as a no-deal trade scenario between the US and China could potentially send the Chinese currency below 7 and that would have a contagion effect onto the rest of Asia.

COMMODITIES

- The growth scare in December led Brent oil prices to extend its November losses, leading to an 8.36% loss over the month. Oil prices were volatile, initially supported by OPEC’s pledge to cut output after the meeting in Vienna before concerns around global growth and rising supply from Russia and US eventually weighed on prices.

- Gold gained significantly over December, rising 5.08% through the month past a key level at $1,250/oz, as markets saw a flight to safety amidst the uncertainties in the month.

- We are bullish on oil prices are see it averaging $70/brl with further upside from here. Our base case is for a Sino-US trade deal, hence reducing concerns of slowing global growth and offering greater clarity into oil demand. OPEC+’s agreement to lower output will officially begin this month and should provide support to oil prices.

- We see technicals supporting Gold from here on and expect it to trade in the range of $1,250 – $1,320/oz.

CONTACT

We would be more than happy to have an informal chat about these and the other services we offer as well as the current opportunities we are looking at.

Dec 12, 2018 | Articles, Global Markets Update

Global equity markets recovered slightly from the October sell-off, with the MSCI All Country World Index ending November +1.30%. However, while investors stuck with equities, global trade and geopolitical events led them to remain defensive. This month saw a continued rotation into defensive sectors like Health Care and Real Estate on the S&P 500, and the Telecommunications, Utilities and F&B sectors on Stoxx 600. The US mid-term election results at the start of the month saw the Democrats take the House while the Republicans retained control of the Senate. This was in line with expectations and helped provide an early boost to the US equity markets.

“Too late to buy equities, too early to buy fixed income (FI)” was a perceptive quote out last week. We think 2019 will be another tricky year after this year given the large number of uncertainties out there and a lack of predictable outcomes. In our view, no one (including the Fed), really knows what might happen to inflation next year with widely polarised views on how many Fed hikes there will be as there are a wide range of inflation expectations.

Markets were also focused on the meeting between Trump and Xi at the G20 summit. The meeting ended with a 90-day truce and set up a framework for future trade talks. We see this truce as a win for both parties in the short-term, given the avoidance of a trade escalation. However, in the longer term, this truce is simply a ‘pause’ in a very complicated dispute and does very little in reducing the substantial differences between China and the US. We remain cautious on whether any of the existing structural issues can be resolved by the end of the 90-day truce. One reason for this is the hostility present within the US administration against China.

Global trade, extending beyond the more well-publicized Sino-US squabble still remains largely uncertain. Sizeable geo-political concerns also remain, with unclear outcomes from Brexit; the Italian budget; Russia’s encroachment on Ukraine; and the powder keg that is the Middle East with its important links to oil prices. In FI, there are opposing views over developments in credit quality and on the favoured spot for duration whilst FX, unlike last year end’s strong consensus behind further USD weakness, appears to have little in the way of conviction.

Depending on the outcomes of these important, but uncertain, outcomes, there could be the need for speedy and material portfolio construction changes. As we’ve seen this year, 2019 could well be another year where making capital gains in equities might prove to be difficult, whilst owning FI might fail to preserve capital. The significant de-rating of equities, despite solid earnings growth bar Asia ex-Japan, provides us with reason to remain more weighted here than in FI, which we still see as a dangerous asset class outside short duration holdings where the risk is not rewarded by the yields. Given the difficulties going forward for traditional asset classes with weaker returns than normal and likely higher volatility, we continue to recommend diversifying into non-traditional asset classes as alternatives and private assets, and the use of significant tactical cash holdings from time to time.

Equities

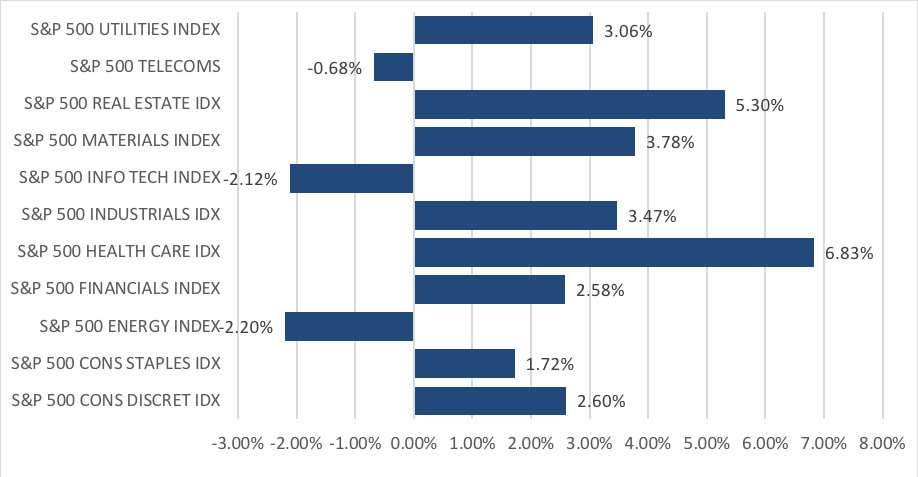

Fig 1: S&P 500 Sector Performance in November Source: Bloomberg

- The S&P 500 gained 1.79%, with Healthcare (+6.83%) and Real Estate (+5.30%) as the biggest gainers in the index which saw gains across most sectors, with the exception of Energy (-2.20%), Info Tech (-2.12%) and Telecommunications (-0.68%). Likewise, the Dow Jones gained 1.68%, while the tech-heavy Nasdaq also managed to gain 0.34% to end the month on a higher close. [Fig 1]

Figure 2: S&P 500 Sector Performance in October

Figure 2: S&P 500 Sector Performance in October

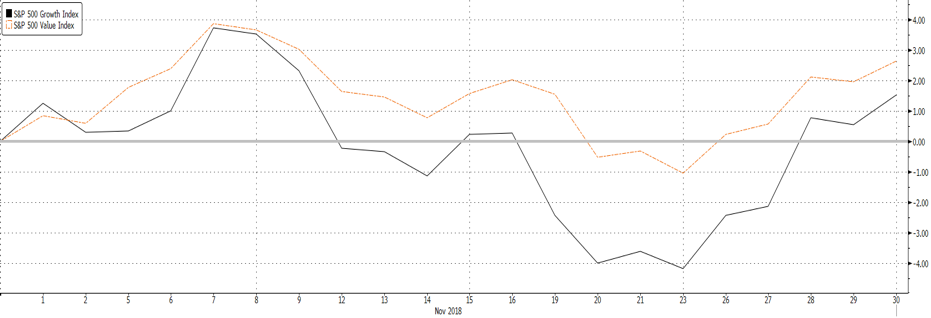

- As we highlighted last month, the divergence between growth and value extended through November, with the SVX Index (Value) closing +2.63% higher and the SGX Index (Growth) trailing behind at +1.53%. [Fig 2]

- Fundamentally, composite lead indicators in the US continue to reflect a strong economy, with nothing to suggest below-trend growth over the next few quarters. The ISM Manufacturing survey came in well above expectations, as production and new orders rebounded from a month ago while export activity held steady and respondents remained confident around business strength.

- GS sees single-digit absolute returns on the S&P 500 for FY19, with the view that US Equities are likely to provide a lower risk-adjusted return compared to its long-term average. In terms of allocation within the US, we are inclined to agree with the GS view to increase exposure to defensive assets within US, as with sectors such as Communication Services and Utilities, and continue to be much more selective when it comes to growth stocks, particularly within IT.

Fig 3: S&P 500 Sector Performance in November Source: Bloomberg

Fig 3: S&P 500 Sector Performance in November Source: Bloomberg

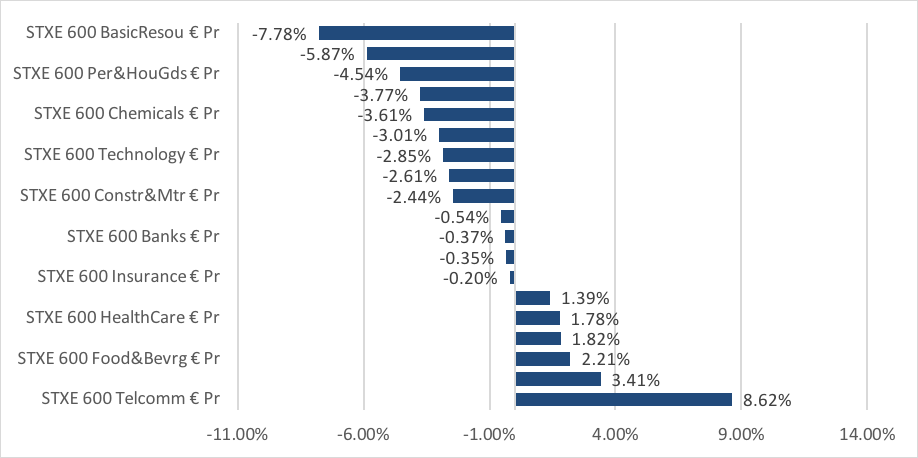

- The Stoxx 600 fell 1.14% in November, but we saw a marked difference in performance across sectors as Telecommunications (+8.62%) and Utilities (+3.41%) outperformed, while Basic Resources (-7.78%) and Oil & Gas (-5.87%) saw steep declines. Given our expectation of elevated political risks next year, we choose to remain underweight Europe in our portfolio allocations. In our view, the risk-reward still remains somewhat lacking in these markets, and until valuations decline lower or we are able to gain some clarity on these issues, we would avoid being too heavily allocated into this region. [Fig 3]

- Asian markets were largely focused around the outcome of the Trump-Xi meeting on the 30th, where the announcement of the 90-day ceasefire sent most Asian markets higher early into December, with the exception of China A-shares which closed -0.57% lower on the month.

- In our view, the agreement between Trump and Xi was more symbolic rather than substantial, and that the Chinese came to the table from a position of weaker bargaining power to provide Xi some relief to focus on the domestic economy.

- The next date to look out for is December 20th, which is scheduled to be the Central Economic Working Conference, where the Politburo’s policymakers are likely to discuss growth and inflation targets for CY19, and any adjustment to policies which they will choose to undertake.

- Ultimately, the question now will be whether China can bring enough to the table to satisfy the U.S.’ concerns around industrial policy & IPR. Our economist foresees a long-drawn negotiation that lies ahead, and what we can expect from that is further market volatility as risks continue to rise around tariffs or threats around them.

- More broadly for Asia ex-Japan, we could very well be looking at the start of a bottoming process which has had seen some uplift from the recent ceasefire in the Sino-US trade conflict. At valuations that float around 11.5x FY19 P/E for MSCI Asia ex-Japan (AxJ), valuations remain at unjustified trough-like levels, which is a prime reason why we have moved from c. 50% to 5% cash in out Asia ex-Japan portfolio, and re-allocated back into what we view as a market with attractive risk-to-reward.

Fixed-Income

- UST yields traded higher earlier in the month after the mid-term elections and on technical factors, with the 2Y yield rising to a high of 2.97% and the 10Y at a high of 3.24%, just above a key resistance level of 3.2% [Fig 4]. However, markets perceived Powell’s speech late in the month to be dovish, causing the UST 10Y yield to fall significantly and end the month at 2.99%, while the 2Y yield finished just 20bps lower at 2.79%. The yield curve continued to flatten into early December.

Fig 4: Flattening yield curve Source: Bloomberg

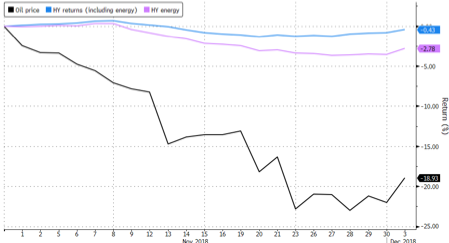

- HY debt continued to lose the most amid concerns of slowing growth globally and in the US. The HY energy sector fell 3.58%, its worst since losing 8.41% in February ‘16 while CCCs led the decline in the general HY sector (Figs 5 & 6).

Fig 5: HY energy sector’s worst month since ’16 Source: Bloomberg

Fig 5: HY energy sector’s worst month since ’16 Source: Bloomberg

Fig 6: CCC debt leads decline Source: Bloomberg

Fig 6: CCC debt leads decline Source: Bloomberg

- The Fed will likely raise rates by another 25bps to 2.25%-2.50% when they meet later this month. Fed fund futures are pricing in a 78.4% probability of that at time of writing. The futures are also pricing in a 75.3% probability that rates will remain at 2.25%-2.50% after January ‘19’s meeting but is more uncertain about a rate increase in March ’19.

- Given the current environment, we recommend staying defensive by allocating to government bonds. We also prefer to remain at the front-end of the curve, given that the current yield spreads do not provide a sufficient yield pick-up to justify the duration risk in longer duration bonds.

- We remain positive on HY debt, albeit less so than in previous months. HY bonds have fallen recently and this pullback came earlier than expected. Yet, there is no sign of a collapse in earnings or an approaching recession. This supports the case that HY debt still remains an attractive asset class, though there is a need to be more selective on the companies we allocate to.

FX

- The USD had a volatile month with mid-term elections, tariff developments, dovish Fedspeak and what markets took to be mixed data releases. December opened with a 90-day ceasefire between Trump and Xi, amidst slowing momentum from October’s stream of strong data.Going into ’19, we expect more sensitivity from the greenback around data releases, given the Fed will also be largely data-dependent.

- The EUR saw a monthly high of 1.145 against the dollar, and a low of 1.12 before ending the month at 1.13, just 3bps from where it started. The EUR remains weighed down by political uncertainty, not least Brexit’s key vote on December 16, and a yet unresolved budget from Italy. It remains to be seen how these headwinds will weigh on the EUR, but we remain more concerned around the GBP which is currently sitting near a critical support at 1.27.

- CNY continued to decline throughout November, but found some artificial support from the 6.97 to 6.95 region before recovering to 6.83 just after the Trump-Xi meeting. Although CNY led most AXJ currencies lower, INR emerged victorious against its peers, ending November higher by +5.90%, supported by cheap oil prices to alleviate its twin deficits.

- Uncertainty around China’s growth given the challenges it will face might cause further doubt on the strength of the CNY. There also remains much uncertainty around EM FX as the spotlight is now on the fragile partnership that is beginning to foster between US and China.

Commodities

- As we draw closer to December’s Vienna meeting, investors have been notably wary with the release of inventory data and news around Russia, Saudi Arabia and potential changes on the supply-side. Despite the sanctions against Iran (albeit with waivers issued to eight nations), November saw Brent plunge from 72.70 (on Nov 1st, Brent fell below its 200DMA for the first time since Aug ’17) to eventually form a short-term support at 59.

- December 2nd’s positive news gave a 5% boost to oil; a trade war ceasefire brought a short lived risk-on appetite to markets; Alberta’s oilfields cut their production by 350,000bbls/day, and the OPEC President hinted a likely production cut during the month.

- Looking ahead, directionality on oil prices could be largely driven by the outcome of the Vienna meeting on 6th Dec.

- In terms of support for Brent crude, we look to three factors in determining our stance 1) Demand is still growing, albeit at a far more muted pace than we had originally expected 2) Supply can and will be cut if necessary, and the OPEC alliance with Russia will be able to do this & 3) The market clearly underprices a risk premium that, in our view, is clearly more evident in the Middle East

- For the factors listed above, we continue to remain bullish on oil prices, with the view that over the next few months, Brent Crude should normalise closer to or above US$70/bbl as opposed to c. US$61 where it sits now.

CONTACT

We would be more than happy to have an informal chat about these and the other services we offer as well as the current opportunities we are looking at.

Nov 9, 2018 | Articles, Global Markets Update

Despite the month-end window dressing, October was a bad month for equities.

Indices in the major regions all closed significantly lower within the range of -5% to -11%, with MSCI AXJ leading declines (Figure 1). This month was also the worst October since ’08, where indices fell in the ranges of -13% to -25%. Markets were risk-off for most of the month, causing a rotation into defensives like Utilities and Consumer Staples in the S&P 500. A similar trend was seen in Stoxx 600, with the F&B, Utilities and Telecomm Services losing the least over the month.

Figure 1: October returns across major indices

Geopolitics and trade concerns continued to weigh in October, starting with the EU formally rejecting Italy’s budget plans, which led to BTP 10Y yields whipsaw around 3.5% while the spread over Bund yields rose to a high of 327bps during the month. Merkel’s decision to not run for re-election as chairman of the CDU in December also renewed political uncertainty in the region and weighed on the EUR. Trade tensions between US and China seemed to improve toward the month-end (and markets took it as such), despite Trump’s threats to levy all remaining Chinese imports if talks with Xi later this month fail.

Corporate earnings were also the focus of this month, as companies are midway through reporting Q3 earnings. As of last week, 74% of companies in the S&P 500 have reported earnings. 78% of these companies have reported earnings beat, while on aggregate, companies are reporting earnings that are 6.8% above the estimates. We saw weaker earnings from US IT stocks like Amazon, Alphabet and Apple, that resulted in overnight losses of c. 4% – 7% while disappointing earnings outlook from industrial bellwethers like Caterpillar and 3M raised concerns around the global growth outlook.

Our base case is founded on the need for an ability to look across the valley as the short-term may see further downside from:

- A possible deterioration of Sino-US relations, with risk that China retaliates via non-trade means such as CNY devaluation etc;

- Weaker EPS outlook and potential Q3 earnings misses – most likely from companies in Asia ex-Japan;

- Cyclical peak in US GDP growth;

- Rising geopolitical risks – notably in Middle East (ME);

- US tariffs on global auto imports; and

- Italy’s budget deficit;

In the medium-term, solid EPS growth in the low double-digits and positive global GDP growth data still underpin the fundamental case for equities. The negatives in the ‘noise’ should not derail EPS or GDP growth but might reduce, on the margin, a more aggressive Fed rate hike cycle for longer. This suggests that the recent correction in equities is one to be adding into selectively, in a disciplined manner.

We think it is highly likely any evidence of a GDP slowdown in 2019 will be met by increased fiscal spending and greater monetary policy gradualism. Rising rates are a risk, but rates are well below levels that have historically disrupted a positive equity trend. In addition, valuations for non-US equities are reasonable and real estate owned recoveries are underway. Even in the US, equity valuations, excluding IT, SMEs and parts of the consumer discretionary/healthcare sectors, are not overly stretched.

As it is almost impossible to finesse market bottoms, we think the only approach has to be to stay the course with relatively defensive positioning and look to become more risk-on as we cross the valley, by being disciplined in adding into further declines while risk managing portfolios, should a rebound take place. Our assumptions are that we do not see a US/global recession in the next 12-18M; that oil prices – bar any Middle East ‘shocks’ – will not move appreciably higher than the mid 80s; and that concerns over global liquidity tightening are exaggerated.

Equities